Frank Palmasani - Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price

Here you can read online Frank Palmasani - Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2013, publisher: Sourcebooks, genre: Home and family. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price

- Author:

- Publisher:Sourcebooks

- Genre:

- Year:2013

- Rating:3 / 5

- Favourites:Add to favourites

- Your mark:

Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

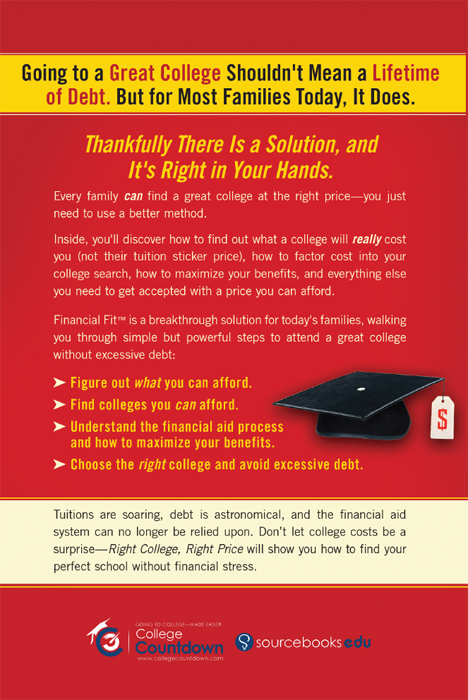

In the midst of a $1 trillion student loan debt crisis, students and their families have had the same question on their minds:

Can I afford to pay for a college education?

Good news: the answer is yes. By shifting the way we think about the college search, every family can find the right college at the right price.

Right College, Right Price helps you discover the real cost of a college (after scholarships, work study, loans, etc.) before you even begin to applysaving you hundreds of dollars in application fees and thousands of dollars in tuition.

This guide will walk you through simple, but powerful, steps of the Financial Fit program, which will allow you to:

With Right College, Right Price, your student will not only have access to a college education, but also a life after collegewithout the burden of excessive student loan debt.

Frank Palmasani: author's other books

Who wrote Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price? Find out the surname, the name of the author of the book and a list of all author's works by series.

Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Copyright 2013 by Frank Palmasani

Cover and internal design 2013 by Sourcebooks, Inc.

Cover Design by The Book Designers

Sourcebooks and the colophon are registered trademarks of Sourcebooks, Inc. Financial Fit and College Affordability Calculator are trademarks of Sourcebooks, Inc.

All rights reserved. No part of this book may be reproduced in any form or by any electronic or mechanical means including information storage and retrieval systemsexcept in the case of brief quotations embodied in critical articles or reviewswithout permission in writing from its publisher, Sourcebooks, Inc.

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.From a Declaration of Principles Jointly Adopted by a Committee of the American Bar Association and a Committee of Publishers and Associations

All brand names and product names used in this book are trademarks, registered trademarks, or trade names of their respective holders. Sourcebooks, Inc., is not associated with any product or vendor in this book.

Published by Sourcebooks, Inc.

P.O. Box 4410, Naperville, Illinois 60567-4410

(630) 961-3900

Fax: (630) 961-2168

www.sourcebooks.com

CIP data is on file with the publisher.

Printed and bound in the United States of America.

VP 10 9 8 7 6 5 4 3 2 1

Part 1

T HE P ROBLEM AND THE S OLUTION

T he way weve been choosing and paying for college for so many years is now broken, leaving families in tough financial situations or with excessive debt. But Im here to tell you that, even faced with soaring tuition, a poor economy, and limited financial assistance, every family can find a great college at the right price. We just need to use a better method.

So much has changed during my thirty-plus years of working with families on selecting and paying for college. Ive always attempted to help them determine how they could provide their son or daughter with the resources to attain a college educationand do it without destroying their own financial lives.

In the early years, the solution was simple: just get families to file forms correctly. Later, it became more complicated: help families understand the details of the financial aid system so that they could better plan, prepare, and learn how to maximize benefits.

But now, in the midst of the student debt crisis and a system gone wrong, these options are simply not good enough for most families. A government financial-aid system that was once the backbone of opportunities for low- and middle-income families can no longer be relied upon to help families solve their problems.

This story is a perfect example of the situation in which many families are finding themselves today.

Jennifer* was a high school senior when she received an official award letter from her top-choice school, Indiana University in Bloomington. However, her award letter listed a net price for the collegewhat her family would have to pay for her to attend after loans and grantsthat was $12,000 more per year than what her family could afford. It was April of her senior year, and Jennifer needed to make a final college decision by May 1. She and her parents had no idea what to do next.

Unfortunately, Jennifers story is common today. Jennifer was a terrific student. Her ACT composite score was 31, and her high school grades were mostly As. But she wasnt given the right approach to make her college choice affordable.

Jennifer believed that she had followed the correct steps during her college search process. After all, she did what high school guidance counselors and college admissions officers told her to do. During her junior year, she and her parents used a well-known and respected college-search software program to help them choose potential colleges. Jennifer focused on colleges in the Midwest that had business programs. When she entered these variables into the program, it generated a list of 327 schools. Jennifer then narrowed down the number of colleges by focusing only on those with an enrollment of 20,000 or more students, because she wanted to go to a large school.

Jennifer wanted to attend a school with a strong business program, so she turned next to U.S. News & World Report. She learned that Indiana University, the University of Illinois, the University of Michigan, and the University of Wisconsin-Madison all had highly respected business programs.

After visiting with college admissions officers at each of these schools, spending time on their websites, and visiting their campuses in the summer between her junior and senior years, Jennifer decided to apply to all four schools. Together, the college applications cost the family $260.

Jennifers guidance counselor and the college admissions officers told Jennifer and her family not to worry about cost. Each college admissions officer suggested that financial aid was available to qualified students and that merit academic scholarships might also be available.

Jennifers parents attended several financial aid sessions at her high school. They learned that, once they filed a financial aid document called the FAFSA, they would receive their Expected Family Contribution (EFC) number. Colleges would use this number to determine how much financial aid the family would receive. Jennifers parents could use this number as a good indicator of how much money they would have to pay out of pocket for her to attend college. Jennifers parents used a program called FAFSA4caster to learn their EFC, which was $12,457. While this amount was high, they believed it was manageable.

Jennifer and her family were also prepared if the net price of college was slightly higher than that EFC number. During the winter of her senior year, Jennifer searched for private scholarships in case additional money was needed. (She was able to obtain a $1,000 one-time scholarship from a local Rotary club.) Her parents also had saved about $6,500 for her college needs. Jennifer was thrilled when she received acceptance letters from all of the four colleges.

However, the shock came in April when the official financial-award letters arrived. None of the schools had a net price anywhere close to the $12,500 that Jennifer and her family had expected. The closest option was their states flagship school, the University of Illinois at Urbana. This school did not offer Jennifer a merit scholarship, and Jennifer only qualified for federal Direct Loans. Thus the colleges net price was $27,500and this appeared to be her best financial option of the four.

Indiana University, Jennifers top-choice college, offered her a merit scholarship. The award letter also indicated that Jennifer qualified for federal Direct Loans, but in the end, the net price was still higher than for the University of Illinois. The two other schools, the University of Michigan and the University of Wisconsin, had net prices that were even higher. So not only was University of Illinois not her first choice in schools, but as the most affordable, it cost more than double what her family could afford.

Extremely disappointed, Jennifer and her family were left with two bad options. She could attend the local community college begrudgingly or she could overextendborrow more than she shouldand attend any of her four options.

Next pageFont size:

Interval:

Bookmark:

Similar books «Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price»

Look at similar books to Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Right College, Right Price: The New System for Discovering the Best College Fit at the Best Price and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.