T. R. Reid - A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System

Here you can read online T. R. Reid - A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2017, publisher: Penguin Press, genre: Politics. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Other rich countries, from Estonia to New Zealand to the UKadvanced, high-tech, free-market democracieshave all devised tax regimes that are equitable, effective, and easy on the taxpayer. But the United States has languished. So byzantine are the current statutes that, by our governments own estimates, Americans spend six billion hours and $10 billion every year preparing and filing their taxes. In the Netherlands that task takes a mere fifteen minutes! Successful American companies like Apple, Caterpillar, and Google effectively pay no tax at all in some instances because of loopholes that allow them to move profits offshore. Indeed, the dysfunctional tax system has become a major cause of economic inequality.

In A Fine Mess, T. R. Reid crisscrosses the globe in search of the exact solutions to these urgent problems. With an uncanny knack for making a complex subject not just accessible but gripping, he investigates what makes good taxation (no, thats not an oxymoron) and brings that knowledge home where it is needed most. Never talking down or reflexively siding with either wing of politics, T. R. Reid presses the case for sensible root-and-branch reforms with a companionable ebullience. This affects everyone. Doing our taxes will never be Americas favorite pastime, but it can and should be so much easier and fairer.

T. R. Reid: author's other books

Who wrote A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System? Find out the surname, the name of the author of the book and a list of all author's works by series.

A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

The Healing of America

The United States of Europe

Confucius Lives Next Door

Heisei Highs and Lows

Tomu no Me, Tomu no Mimi

Ski Japan!

The Chip

Congressional Odyssey

PENGUIN PRESS

An imprint of Penguin Random House LLC

375 Hudson Street

New York, New York 10014

penguin.com

Copyright 2017 by T. R. Reid

Penguin supports copyright. Copyright fuels creativity, encourages diverse voices, promotes free speech, and creates a vibrant culture. Thank you for buying an authorized edition of this book and for complying with copyright laws by not reproducing, scanning, or distributing any part of it in any form without permission. You are supporting writers and allowing Penguin to continue to publish books for every reader.

Cartoon by Jeff MacNelly, courtesy of Gallery on Greene

ISBN 9781594205514 (hardcover)

ISBN 9780735223967 (e-book)

Version_1

Filio filiabusque in amore dedicatus

The members of the U.S. Senate rose to their feet and erupted into cheers, handshakes, and hugs on September 7, 1913, to celebrate final passage of the Underwood-Simmons Tariff Actthe statute that created Americas federal income tax. Determined to milk the moment for maximum political benefit, President Woodrow Wilson held a formal signing ceremony at the White House and told the assembled reporters he was proud to be present at the creation of this highly popular tax.

Back then, the newly minted federal income tax was popular with almost all Americans because hardly any had to pay it. The tax we love to hate today was initially aimed squarely at the silk-suit-and-satin-gown setthe Astors and Vanderbilts, the Morgans and Rockefellers. Only the richest smidgen of the population had to file a return, and even for them the top tax rate was just 7%. Over the next nine years, Congress tinkered with the tax regime, each year passing a new internal revenue code with exemptions and exclusions; the deduction for charitable contributions, for example, was added in 1917. The top rate went up sharply to pay for World War I and then came down again. Eventually, in the Internal Revenue Code of 1922, the structure of the federal income tax was essentially set. There were new revenue acts every few years1932, 1939, 1946but the basic system stayed in place for three decades.

By the 1950s, everyone agreed that the Internal Revenue Code was a complex, confusing, contradictory mess. The new president, Dwight Eisenhower, demanded reformand Congress obliged with a complete rewrite: the Internal Revenue Code of 1954. Among much else, it set the deadline for filing your income tax return on April 15. This code stayed in place for three decades, but almost every year Congress, of course, added exclusions and credits and allowances in a haphazard fashion.

By the mid-1980s, the code was such a voluminous, complicated monster that a conservative Republican president and a liberal Democratic Speaker of the House agreed to another complete rewrite: the Internal Revenue Code of 1986. The economists loved this one; it was a comprehensive revision based on the most fundamental principle of sound tax writing.

Theres a pattern here. In the thirty-two years from 1922 to 1954, the Internal Revenue Code became such a chaotic muddle that it had to be replaced. In the thirty-two years from 1954 to 1986, history repeated itself, and once again the Internal Revenue Code had to be rewritten.

It has now been three decades since the last revision. Everyone agrees once again that our nations basic tax law has become a fine mess: so absurdly complex, so byzantine, that it has to be completely revised. Following the historical patternevery thirty-two yearsthe next major revision should come in 2018. Which means Congress and the president have to start working in 2017 to revamp the Internal Revenue Code.

But what should be in this new tax code? Can we make the U.S. tax system simpler, fairer, and more efficient? The answers: yes, yes, and yes. Could we cut tax rates and still bring in more revenue? Yes. We know this because there are good models all over the world to show us how to do it. Other rich countries like oursadvanced, high-tech, free-market democracieshave devised tax regimes that are equitable, effective, and easy on the taxpayer (although theyve made some serious blunders as well). By looking at tax systems around the world, we can learn what the United States should and shouldnt do in writing the Internal Revenue Code of 2018.

D uring one of its periodic bursts of anger at the Internal Revenue Service, the U.S. Congress passed a strict new law requiring the Treasury Department to reduce the complexity of Americas income tax system. In standard congressional fashion, this mandate for simplicityits known as the anti-complexity clausewas included in a massively complex piece of legislation that added some thirty thousand words and scores of complicated new deductions, exemptions, and credits to the bloated multivolume corpus of the nations tax law. If you happen to be browsing through the statute books some restless night, you can find the anti-complexity clause in Subsection IX of subpart (ii) of Section 7803(c)(2)(B) of the Internal Revenue Code.

Its classic: Congress decides to reduce the complexity of our tax code by making it even more complex. It might be funny if the whole taxpaying process in America werent so maddeningly expensive, inefficient, and time-consuming. At the same time Congress took that principled stand in favor of simplicity, it also added a clausethat would be Section 7803(c)(2)(B)(ii)(III)requiring that Treasury file a report each year on the overall cost of the income tax regime. The reported burden on U.S. taxpayers turns out to be no laughing matter.

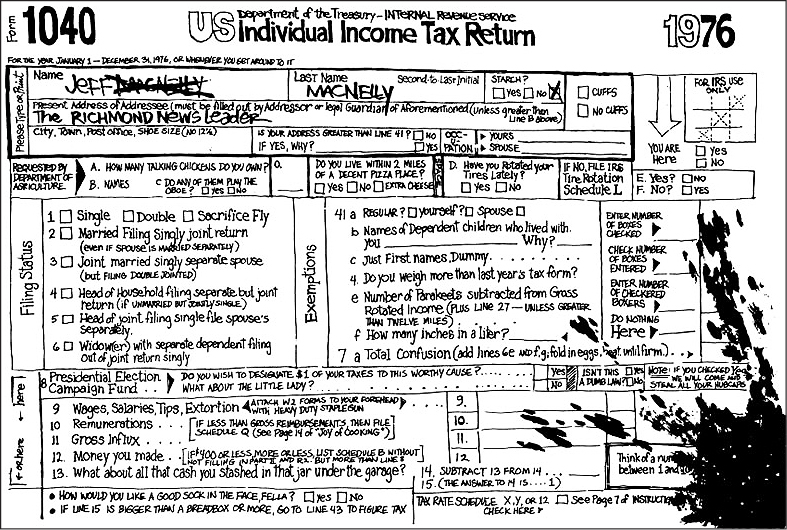

In 2015, the government estimates, American taxpayers spent just over six billion hours preparing and filing their income tax returns. They paid $10.1 billion in fees to the booming tax-preparation industry and another $2 billion for tax software programs (programs that still require hours of work for the typical taxpaying household). For an American household earning the median family incomeabout $55,000the average is more than thirty hours per year gathering documents and filling out forms. Tens of millions of Americans have to spend the weekend before April 15a lovely spring interlude when they should be out on the golf course or at the kids soccer gametearing their hair out over instructions like this gem from IRS Form 1041: Go to Part IV of Schedule I to figure line 52 if the estate or trust has qualified dividends or has a gain on lines 18a and 19 of column (2) of Schedule D (Form 1041) (as refigured for the AMT, if necessary).

T HE CARTOONIST J EFF M AC N ELLY used to offer a satire of this process every April 15:

Visit bit.ly/2mMukOA for a larger version of this image.

It doesnt have to be this way.

If you walk down the street in London, Tokyo, Paris, or Lima, you wont see an office of H&R Block or any similar firm; in other nations, people dont need a tax-preparation industry to file their returns. Parliaments and tax collection bureaus all over the world have done what the U.S. Congress seems totally unable to do: theyve made paying taxes easy.

Font size:

Interval:

Bookmark:

Similar books «A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System»

Look at similar books to A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book A Fine Mess: A Global Quest for a Simpler, Fairer, and More Efficient Tax System and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.