BPP Learning Media (Firm) - IFRS explained

Here you can read online BPP Learning Media (Firm) - IFRS explained full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. City: London, year: 2010, publisher: BPP Learning Media, genre: Romance novel. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:IFRS explained

- Author:

- Publisher:BPP Learning Media

- Genre:

- Year:2010

- City:London

- Rating:5 / 5

- Favourites:Add to favourites

- Your mark:

IFRS explained: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "IFRS explained" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

IFRS Explained goes over the background to IFRS and sets out the provisions of the standards clearly, with working and examples to illustrate the main points. The standards themselves are detailed, technical and in some cases quite extensive. This book can be used alone or as a companion to the standards, making it easier to navigate the technical detail.

This book will be a valuable resource for accountants preparing financial statements under IFRS, students doing accountancy degrees or the professional exams and anybody who needs to gain an understanding of IFRS.

BPP Learning Media (Firm): author's other books

Who wrote IFRS explained? Find out the surname, the name of the author of the book and a list of all author's works by series.

IFRS explained — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "IFRS explained" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

IFRS Explained

First edition 2010

ISBN 978-0-7517-8630-9 Master e-book ISBN

ISBN 9780 7517 8545 6

British Library Cataloguing-in-Publication Data

A catalogue record for this book is available from the British Library

Published by

BPP Learning Media Ltd

BPP House, Aldine Place

London W12 8AA

www.bpp.com/learningmedia

Printed in Malta

Printed on paper sourced from sustainable, managed forests.

All our rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of BPP Learning Media Ltd.

BPP Learning Media Ltd

2010

Page |

Part A:The regulatory and conceptual framework |

Part B:Single entity financial statements |

Part C:Group financial statements |

Part D:Specialised standards |

This book is intended for those with basic accounting knowledge who now wish to get familiar with IFRS. We have dealt with the standards under topic headings and the aim has been to show how the provisions of the standards are applied in practice. Rather than detailed cross-references to sections and sub-sections, we have concentrated on bringing out the key points and showing examples and workings where applicable.

We have explained in some detail the preparation of IFRS financial statements including consolidated financial statements. Many readers will already be familiar with consolidation procedures, but may find it useful to go through the basics before taking account of those issues peculiar to IFRS, such as non-controlling interest at fair value.

We have omitted two standards dealing with financial reporting by financial institutions:

IAS 26 Accounting and Reporting by Retirement Benefit Plans

IFRS 4 Insurance Contracts

These are complex standards and knowledge of them is not required by most preparers of financial statements.

The IASB and the regulatory framework

The current reality is that the worlds capital markets operate more and more freely across borders. The impacts of rapid globalisation are epitomised by the words of Paul Volker, Chairman of the IASC Foundation Trustees in November 2002, in a speech to the World Congress of Accountants.

Developments over the past year and more have strongly reinforced the logic of achieving and implementing high-quality international accounting standards. In an age when capital flows freely across borders, it simply makes sense to account for economic transactions, whether they occur in the Americas, Asia, or Europe, in the same manner. Providing improved transparency and comparability will certainly help ensure that capital is allocated efficiently. Not so incidentally, generally accepted international standards will reduce the cost of compliance with multiple national standards.

As the modern business imperative moves towards the globalisation of operations and activities, there is an underlying commercial logic that also requires a truly global capital market. Harmonised financial reporting standards are intended to provide:

A platform for wider investment choice

A more efficient capital market

Lower cost of capital

Enhanced business development

Globally, users of financial statements need transparent and comparative information to help them make economic decisions.

From 2005 EU listed companies have been required to use IAS/IFRS in preparing their consolidated financial statements. This is an important step towards eventual harmonisation with the US.

The International Accounting Standards Board is an independent, privately-funded accounting standard setter based in London. Contributors include major accounting firms, private financial institutions, industrial companies throughout the world, central and development banks, and other international and professional organisations.

In March 2001 the IASC Foundation was formed as a not-for-profit corporation incorporated in the USA. The IASC Foundation is the parent entity of the IASB.

From April 2001 the IASB assumed accounting standard setting responsibilities from its predecessor body, the International Accounting Standards Committee (IASC). This restructuring was based upon the recommendations made in the Recommendations on Shaping IASC for the Future. In essence, the restructuring was driven by the need to increase the level of resourcing owing to an increasing workload.

The 15 members of the IASB come from nine countries and have a variety of backgrounds with a mix of auditors, preparers of financial statements, users of financial statements and an academic.

The formal objectives of the IASB are to:

(a) Develop, in the public interest, a single set of high quality, understandable and enforceable global accounting standards that require high quality, transparent and comparable information in financial statements and other financial reporting to help participants in the various capital markets of the world and other users of the information to make economic decisions

(b) Promote the use and rigorous application of those standards

(c) Work actively with national standard-setters to bring about convergence of national accounting standards and IFRSs to high quality solutions

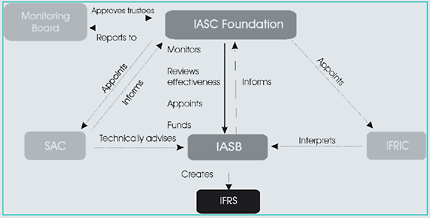

The structure of the IASB can be illustrated by the following diagram:

The IASC Foundation is made up of 22 Trustees, who essentially monitor and fund the IASB, the SAC and the IFRIC. The Trustees are appointed from a variety of geographic and functional backgrounds according to the following procedure:

(a) The International Federation of Accountants (IFAC) suggested candidates to fill five of the Trustee seats and international organisations of preparers, users and academics each suggested one candidate.

(b) The remaining Trustees are at-large in that they were not selected through the constituency nomination process.

The SAC is essentially a forum used by the IASB to consult with the outside world. It consults with national standard setters, academics, user groups and a host of other interested parties to advise the IASB on a range of issues, from the IASBs work programme for developing new IFRSs, to giving practical advice on the implementation of particular standards.

IFRIC provides guidance on specific practical issues in the interpretation of IFRSs. The IFRIC is discussed in more detail below.

The IASB achieves its objectives primarily by developing and publishing IFRSs and promoting the use of those standards in general purpose financial statements and other financial reporting.

Font size:

Interval:

Bookmark:

Similar books «IFRS explained»

Look at similar books to IFRS explained. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book IFRS explained and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.