ClydeBank Business - LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies

Here you can read online ClydeBank Business - LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2017, publisher: ClydeBank Media LLC, genre: Romance novel. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies

- Author:

- Publisher:ClydeBank Media LLC

- Genre:

- Year:2017

- Rating:5 / 5

- Favourites:Add to favourites

- Your mark:

LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Is forming an LLC (Limited Liability Company) the right move for your business? How much do LLCs actually protect you? And what do you stand to gain from a tax perspective? The intricacies and opportunities involved in forming and operating an LLC are now simplified thanks to the LLC QuickStart Guide from ClydeBank Business.

It only takes one lawsuit to financially devastate an up-and-coming entrepreneur. LLCs were created to give business owners the liability protections of a corporation with the simplified tax obligations of a proprietorship or partnership. The flexibility and protective qualities of LLCs have made them the business entity of choice for countless successful ventures. Though theyve only been in existence for four decades, LLCs have rapidly evolved and diversified to accommodate everything from single-owner small businesses to sprawling global conglomerates.

Consider this LLC QuickStart Guide form ClydeBank Business your executive briefing on the pros, cons, ins and outs of LLC formation. Whether youre a high net-worth business owner looking to protect your personal assets, or a newly minted entrepreneur seeking an improved basic understanding of how LLCs function, this LLC QuickStart Guide will provide key information in a readable, easy-to-follow format.

Youll Learn:

ClydeBank Business: author's other books

Who wrote LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies? Find out the surname, the name of the author of the book and a list of all author's works by series.

LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Contents

Terms displayed in bold italic can be found defined in the glossary

DOWNLOAD YOUR FREE DIGITAL ASSETS!

Visit the URL below to access your free Digital Asset files that are included with the purchase of this book.

DOWNLOAD YOURS HERE:

www.clydebankmedia.com/llc-assets

Introduction

LLCs (Limited Liability Companies) are becoming increasingly popular. Aspiring entrepreneurs and small business owners catch wind of them, l earn that they can be used to limit their personal liabilities in the event of a major business disaster and think, Hmmm, this almost sounds like a free form of business loss insurance ... and, to some extent, theyre right.

While an LLC offers tremendous advantages as a structure for businesses, understanding the appropriate steps to take in starting one and whats really transpiring, in a legal sense, can require a lot of explaining. The intent of this book is to provide a sound understanding of how an LLC is formed, how it operates, and how it can be leveraged for the greatest benefit for your small business.

You may be wondering if a book and a little Internet research will adequately prepare you for setting up your LLC. Heres the deal: LLCs are a relatively new type of business structure. In fact, the first LLC was started less than 40 years ago in Wyoming. It was introduced as a mechanism to remedy what were perceived as shortcomings in other business structure formats, and the void it fillsin the business senseis often a benefit to those who elect to take advantage of the LLC format.

The idea of the LLC caught on, and by the 1990s LLCs could be formed in every state. Thats the other thing about LLCs: theyre formed within the state. You cant just go into business at-will, as you would with a sole proprietorship or a partnership. You have to file Articles of Organization in the state of your choice. Well talk more about how to choose the right state for your LLC in Chapter 6. The basics of the LLC are similar from state to state, but not identical. Were going to cover the the more universal elements of LLCs, while being sure to direct you towards resources with more state-specific information.

| 1 | LLC Basics

Since the LLC is a newer form of business entity, theres still a lot to be decided by the courts when it comes to how LLCs operate under the law. So, the safest answer to this question is yes, but, as you can probably infer, thats also the most expensive option. With each passing year, and as more and more case law is generated that helps us understand the role of LLCs in the business environment, its become easier and easier to do things on your own. Were living in an age in which its easy to find great books (like this one!) and sophisticated online tools (such as legalzoom.com [no affiliation]). These inexpensive and at times free resources may provide sufficient information for certain individuals in certain states. Other individuals may find that the best option is to hire an attorney to help walk them through the process of forming an LLC.

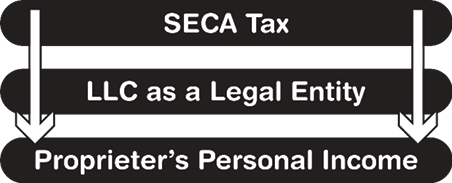

If you dont already understand the concept of pass-through taxation, then it is a good idea to get your head around it before you delve too deeply into this analysis of LLCs. Pass-through taxation refers to the taxing of business income through the taxing of personal income. Its one of the fundamental factors that distinguishes LLCs and sole proprietorships from corporations; LLCs and sole proprietorships are subject to pass-through taxation. The business entity itself isnt taxed, but the business earnings are taxed as part of the owners individual personal income.

Note : When business income is taxed via pass-through taxation, the business entity itself is classified by the IRS as a disregarded entity , meaning, an entity that exists but is not directly taxed.

Pass-through taxation isnt necessarily a bad thing, but it can definitely be more expensive than corporate taxation. In fact, whenever you ask your lawyer to review the negatives of the LLC model, this usually tops the list. Heres why: when a corporations profits are taxed, Medicare and Social Security taxes arent imposed (1.45% and 6.2%, respectively). For corporations, these types of taxes are only imposed on the salaries the corporation pays to its employees. When a person is acting as a sole proprietor, or when a group of people is acting as an LLC, their business profit is subject to Medicare and Social Security, as well as standard federal, state and local taxes. Pass-through taxation operates just like self-employment tax , so the LLC owner or partner is paying the full portion of his Social Security and Medicare obligations in taxes, as opposed to splitting these tax burdens with his employer.

Note : Ordinarily, when an individual is working for an employer, the employer pays 50% of the federally-required Medicare and Social Security withholdings. When an individual is classified as self-employed, he or she is responsible for paying 100% of the federal withholding. This Social Security funding tax is known as SECA, instead of FICASelf Employed Contributions Act and Federal Insurance Contributions Act, respectively. The good news for small business owners is that your employer portion of the SECA tax (50%) can be written off.

Its important to point out here that LLCs can opt to be taxed as corporations. Well go into further detail on taxation in Chapter 5.

One of the problems with the general publics current understanding of LLCs is that theyre not all that clear on the downsides. Why stick with a sole proprietorship or a partnership when you can be absolved from all debt and legal liability with an LLC? In some ways it really is true, even though it may seem too good to be true. LLCs are awesome!

When you form an LLC, you and your co-founders or co-owners will only put at risk the money and the financial assets that you contribute to the LLC. If the LLC gets into trouble and cant pay its debts, or if someone wages a lawsuit against your LLC and wins, then theyre not going to get your house, your car, or anything out of your personal bank account.

What this means for you is if you have very little money in the bank, what you dont put into your business is protected. On the other hand, if youve got a lot of assets, a high net worth, etc., and you want to open up a construction company, then you should seriously consider going with an LLC to keep your personal assets safe in the event of an on-the-job accident or some other unforeseen event that ends up exerting a serious financial burden on your business. Many view this as a win-win situation. Every business person understands that he shouldnt invest more that he is willing to lose, and an LLC essentially guarantees that what he elects not to invest stays safe.

If youre just looking to devote yourself to the humble but delicious pursuit of being a donut shop owner, you could go the LLC route, but getting started is going to be a lot more time consuming and expensive. This is the chief setback of the LLC structure; when starting a sole proprietorship, you can pretty much just get up and go into business. Youll have to make sure you have the proper licensure and permits, and youll need to keep track of your earnings for tax purposes, but thats really about it.

Font size:

Interval:

Bookmark:

Similar books «LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies»

Look at similar books to LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book LLC QuickStart Guide: The Simplified Beginners Guide to Limited Liability Companies and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.