Erdmann - Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy

Here you can read online Erdmann - Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. City: United States, year: 2019, publisher: Rowman & Littlefield Publishers, genre: Business. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Erdmann: author's other books

Who wrote Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy? Find out the surname, the name of the author of the book and a list of all author's works by series.

Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Kevin Erdmann was a small business owner for 17 years. In 2010, he sold his business and earned his masters degree in finance from the University of Arizona, which grounded his real-world experience of investing in the rigor of the academy.

In 2013, he began blogging at idiosyncraticwhisk.com to share his contrarian observations about investment strategies and research. He was surprised to uncover evidence that seemed to contradict conventional narrative and common assumptions about the housing bubble and the financial crisis. As the evidence accumulated, he developed a new account of the causes of the housing bubble and financial crisis. That account eventually became a two-book project, Shut Out and a follow-up book still in development, both of which synthesize and expand on the housing theories he originally published on his blog.

He lives in Gilbert, Arizona, with his wife and three kids.

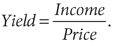

The different mental frameworks we use when we think about different classes of assets have a significant effect on our response to changing values. We think of bonds in terms of yield. This is because bonds tend to be issued at a standard face value (say, $100), and so bond buyers think in terms of how much income they will receive for each $100 investment. Newly issued bonds have a fixed price, so when market yields change, it is cash flows that adjust. If yields were 3% last year and are 2% this year, then bondholders in both years think of their investment as a $100 investment that last year earned $3 and this year earns $2. But, for long-term bonds that were issued last year, the bonds market value will rise substantially in the second year as a result of those falling yields. When new bonds only fetch $2, existing bonds that pay $3 are worth much more than $100.

Since bonds tend to differ in maturity dates, so that a yield change affects each bonds price differently, it is easier to think of bond markets in general in terms of yield, and then to apply that yield to each individual bond to estimate the price.

But, since homes have no maturity date, if they are properly updated and maintained, they are essentially perpetuities. This means that changing yields have a similar effect on all home prices. Furthermore, rents are very stable in the short term. When yields change on bonds, cash flows change along with them. But when yields change on homes, rents remain stable. This means that price is the variable that must change in response to short-term changes in yield. So, in homes, we think in terms of price.

These different mental framings lead us to discuss bonds and homes in opposite ways. Any change in yield on any financial security reflects a transfer between future owners and past owners. When yields decline, past owners receive a capital gain on the basis of the changing market value, and future owners receive lower incomes on the basis of falling yields. But these are mathematically two sides of the same coin. Price is the inverse of yield:

So, when yields fall, we think of homes as having rising prices, and we note that owners have gained wealth, even though their rental incomes have not changed. (In fact, in Open Access cities, their rental incomes should fall as new capital is attracted into the homebuilding market, increasing the competition for rents.) At the same time, we think of bondholders as losing, and public discussions revolve around the problem of savers and pensioners receiving lower incomes. But, at least if we compare homeowners to owners of very long-term bonds, we are basically describing the same circumstances.

If we presume that homebuyers are simply agents of demand, with no rational pricing discipline, then it is easy for this mental framing to lead us to conclude that increases in home prices are temporary outcomes of having too much credit or too much money. In that case, it would look like high home prices created a wealth effect where house holds were enticed into spending more than they really could afford, because their inflated home values caused them to overestimate their wealth.

However, if we presume that home prices do tend toward no arbitrage prices (in the loose sense) relative to other assets, then this is a case where the cause of the price change is important. If the price change is due to changing yields, then the wealth effect is probably not significant, especially in Open Access cities where building will be triggered. But if the price change is due to rising rents, then the wealth effect is not temporary. Then the wealth effect reflects higher income expectations from future rents. Since rising local rents for entire metropolitan areas are only sustainable over the long term when they are paired with rising local incomes, the rising rents themselves reflect higher incomes.

The Reserve Bank of Australia has done research on this topic, finding that when home prices increased, instead of seeing a pure wealth effect among only homeowners, both owners and renters increased their spending. The conclusion... is that it is a common third factor such as higher expected future income, or less income uncertainty, that is, at least partly, responsible for the observed association between housing wealth and spending.

While incomes and expected incomes are an important factor in home prices, there are natural factors that moderate prices. Since homes cannot be easily purchased piecemeal, as one might purchase shares of a firm, access to credit serves as an obstacle to demand. People with only a small amount of savings can buy a few shares of Berkshire Hathaway or a mutual fund more easily than they can buy real estate.

High transaction costs also limit demand for homeownership. High transaction costs mean that if prospective buyers expect to live in a home for less than several years, the expected return to buying a home is probably not worth the purchase cost.

This factor limits demand, pulling owner-occupied home values down, making values dependent on tenancy. The longer an owner lives in a home, the higher the yield will be on his or her investment, after transaction costs.

There is a similar effect in the market for firms. Privately held firms usually sell at a discount. In other words, they earn a higher return for their investors. And the reason they do is that it is more difficult to find a buyer for such firms. Google, on the other hand, can be bought and sold in bits and pieces, by investors who can even buy shares with borrowed money. So a firm like Google trades at nearly its full value, with little discount required to account for liquidity. The market for Google shares is very liquid, so the return on investment for speculators that hold shares for weeks or months isnt much less than the return on investment for long-term holders.

The effect of transaction costs and market liquidity is asymmetrical. Adding costs can lower the price and raise the yield of a security, but once a market is sufficiently liquid, adding more liquidity will not continue to boost the price. If brokers decided that Google could be traded with a margin account leveraged up to 90%, this wouldnt move the price of shares much, because there are many potential sellers who will sell shares when they think the price is too high.

This same asymmetry applies to housing markets. Homeowners may be less likely to sell, for personal reasons or because of the high cost, so there is some additional danger of added liquidity pushing home prices above a sustainable level, where yields on investment are temporarily lower than they are for assets with similar risks. But the flight of homeowners out of Closed Access cities and the decline in the national homeownership rate that began a couple of years before prices peaked suggests that there are sellers willing to react to rising prices.

Font size:

Interval:

Bookmark:

Similar books «Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy»

Look at similar books to Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Shut Out: How a Housing Shortage Caused the Great Recession and Crippled Our Economy and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.