Slava Gomzin - Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions

Here you can read online Slava Gomzin - Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2014, publisher: Wiley, genre: Computer. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions

- Author:

- Publisher:Wiley

- Genre:

- Year:2014

- Rating:4 / 5

- Favourites:Add to favourites

- Your mark:

Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Must-have guide for professionals responsible for securing credit and debit card transactions

As recent breaches like Target and Neiman Marcus show, payment card information is involved in more security breaches than any other data type. In too many places, sensitive card data is simply not protected adequately. Hacking Point of Sale is a compelling book that tackles this enormous problem head-on. Exploring all aspects of the problem in detail - from how attacks are structured to the structure of magnetic strips to point-to-point encryption, and more its packed with practical recommendations. This terrific resource goes beyond standard PCI compliance guides to offer real solutions on how to achieve better security at the point of sale.

- A unique book on credit and debit card security, with an emphasis on point-to-point encryption of payment transactions (P2PE) from standards to design to application

- Explores all groups of security standards applicable to payment applications, including PCI, FIPS, ANSI, EMV, and ISO

- Explains how protected areas are hacked and how hackers spot vulnerabilities

- Proposes defensive maneuvers, such as introducing cryptography to payment applications and better securing application code

Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions is essential reading for security providers, software architects, consultants, and other professionals charged with addressing this serious problem.

Slava Gomzin: author's other books

Who wrote Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions? Find out the surname, the name of the author of the book and a list of all author's works by series.

Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Science in the service of humanity is technology, but lack of wisdom may make the service harmful.

Isaac Asimov

Because people have no thoughts to deal in, they deal cards, and try and win one another's money. Idiots!

Arthur Schopenhauer

In order to understand the vulnerability points of point-of-sale and payment applications, it is necessary to know the basicshow, when, and why sensitive cardholder data moves between different peers during the payment transaction cycle:

- Why (the reason): Is it really necessary to hold, store, and transmit this data throughout the entire process?

- How (the location and the routes): What are the areas with a concentration of sensitive records?

- When (the timing): How long is this information available in those areas?

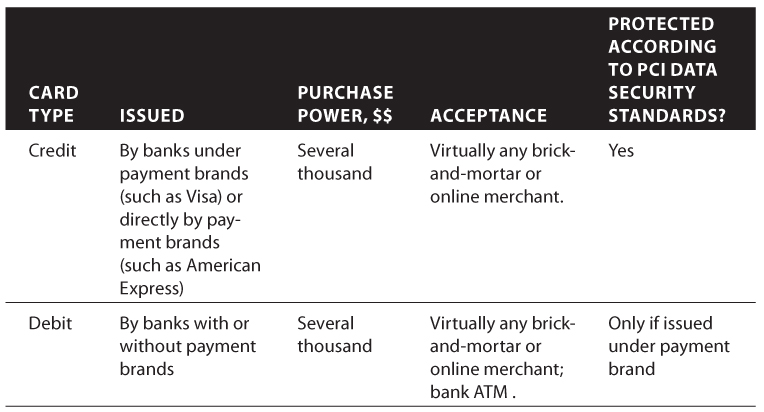

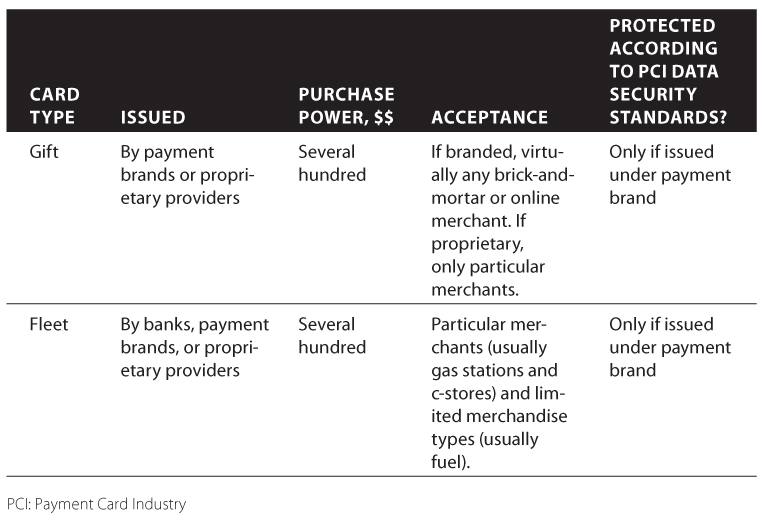

The use of payment cards is obviously one of the main subjects of this book. There are several main types of payment cards commonly used for payments:

shows a list of major payment card types and their main features.

Payment Card Types

There are two main methods used to enter the card data into the POS in order to start a payment transaction: swipe and manual entry.

The first method uses a Magnetic Stripe Reader, or MSR, which is a device that reads the magnetic stripe on payment cards. Modern MSR devices have encryption capabilities and can be used in point-to-point encryption (P2PE) solutions (see Chapter 8 for more details). The easiest way to enter the card data into the POS is to just swipe the card in the MSR so it can read the magnetic stripe and automatically enter all the necessary information. However, if the magnetic stripe is damaged, the customer or cashier can manually enter the account number and expiration date embossed on the front of the card.

Some MSR devices emulate keyboard input, so swiping the card is equivalent to simply typing numbers and letters on the computer keyboard. Stealing the track data in this case is as simple as sniffing the MSR input by installing a keystroke logger.

The second method uses a pinpad. A pinpad, or Point of Interaction (POI) with a built-in MSR, is a more sophisticated device because it has firmware which can be customized for various functions including protection of the card's sensitive data. Most pinpads also have hardware encryption capabilities implemented as TRSM (Tamper-Resistant Security Module). In addition to MSR, POI also includes other peripherals, such as a customer display and keyboard (in addition to the pinpad), for better direct interaction with the customer throughout the payment process.

According to Visa, there are five key players in the card payment processing game: Consumers, Merchants, Acquirers, Issuers, and Card Brands. However, in practice, there are usually more participants. In addition to Consumers, Merchants, Acquirers, Issuers, and Card Brands, there are also Gateways, Processors, Software Vendors, and Hardware Manufacturers who facilitate the payment transaction processing.

Before diving into the details of these players, I would like to remind you that the scope of this book is security of POS and associated payment applications which are located in brick-and-mortar stores. Despite the fact that merchants account for a relatively small percentage of the overall payment processing life cycle, their portion of responsibility and risk is incomparably larger than anyone else's share. There are several reasons for this:

It's us. We go to stores, swipe the cards, and pay the bills.

Ideally, consumers are not supposed to care about security beyond keeping their PIN a secret. If the card is lost or stolen, the consumer just wants to call the bank and get a new one. When our card is swiped, our private information is shared with the merchant, whose POS system is supposed to protect our information throughout the process. We rely on modern high-end technologies to protect our plastic money.

Next pageFont size:

Interval:

Bookmark:

Similar books «Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions»

Look at similar books to Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Hacking Point of Sale: Payment Application Secrets, Threats, and Solutions and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.