Allison J. Harrell - Yellow Book: Government Auditing Standards

Here you can read online Allison J. Harrell - Yellow Book: Government Auditing Standards full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2018, publisher: Wiley, genre: Politics. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Yellow Book: Government Auditing Standards

- Author:

- Publisher:Wiley

- Genre:

- Year:2018

- Rating:3 / 5

- Favourites:Add to favourites

- Your mark:

Yellow Book: Government Auditing Standards: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Yellow Book: Government Auditing Standards" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Do you perform engagements in accordance with generally accepted government auditing standards (GAGAS) as presented in the Yellow Book? This book provides an excellent baseline of information for accountants to better understand governmental auditing foundations, ethics, general audit standards, financial audit standards, attestation engagement standards, and fieldwork and reporting standards for performance audits. It is essential that all auditors planning and conducting audits in accordance with GAGAS understand and discern these concepts and standards in executing their responsibilities.

In addition to a chapter covering the key points in a Uniform Guidance compliance audit, this book also includes content from AICPA Guide Government Auditing Standards and Single Audits related to a Uniform Guidance compliance audit, including appendixes for example auditors reports and sampling guidance.

This book will prepare you to do the following:

Allison J. Harrell: author's other books

Who wrote Yellow Book: Government Auditing Standards? Find out the surname, the name of the author of the book and a list of all author's works by series.

Yellow Book: Government Auditing Standards — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Yellow Book: Government Auditing Standards" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Notice to Readers

Yellow Book: Government Auditing Standards is intended solely for use in continuing professional education and not as a reference. It does not represent an official position of the Association of International Certified Professional Accountants, and it is distributed with the understanding that the author and publisher are not rendering legal, accounting, or other professional services in the publication. This course is intended to be an overview of the topics discussed within, and the author has made every attempt to verify the completeness and accuracy of the information herein. However, neither the author nor publisher can guarantee the applicability of the information found herein. If legal advice or other expert assistance is required, the services of a competent professional should be sought.

You can qualify to earn free CPE through our pilot testing program. If interested, please visit aicpa.org at http://apps.aicpa.org/secure/CPESurvey.aspx.

2017 Association of International Certified Professional Accountants, Inc. All rights reserved.

For information about the procedure for requesting permission to make copies of any part of this work, please email with your request. Otherwise, requests should be written and mailed to Permissions Department, 220 Leigh Farm Road, Durham, NC 27707-8110 USA.

Course Code: 736127

EO-YB GS-0417-0B

Revised: April 2017

G ENERALLY A CCEPTED G OVERNMENT A UDITING S TANDARDS (Y ELLOW B OOK )

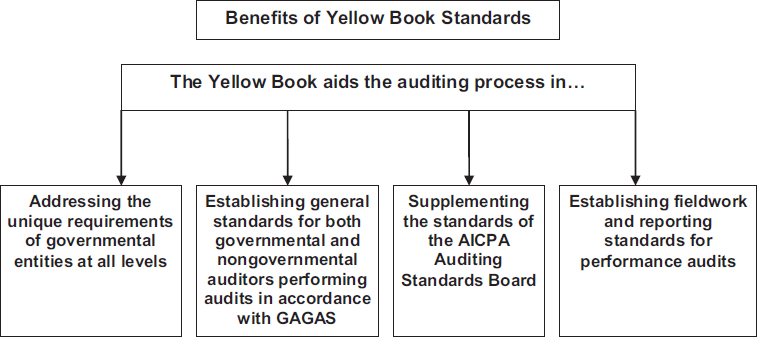

Generally accepted government auditing standards (GAGAS), issued by the U.S. Government Accountability Office (GAO), is the statement of auditing standards for audits of government organizations, functions, activities, and programs, as well as for government assistance received by nonfederal entities. The requirements of GAGAS apply to audits of governmental entities, programs, activities, and functions of government assistance administered by contactors, nonfederal entities, and other entities when the use of GAGAS is required or voluntarily followed. Known widely as the Yellow Book, GAGAS aids the auditing process in the following four ways:

To meet ongoing demands for more responsive and cost-effective government, policy makers and managers need reliable financial and performance information. The assurance that auditors provide about that information, as well as about the internal processes that produce it, is a critical component of fiscal integrity and accountability. GAGAS help provide accountability and assistance to public officials and employees in carrying out their responsibilities. Auditing provides credibility to the information reported by, or obtained by, management.

The terms GAS and GAGAS are often used interchangeably; however, in this course, the terms GAS, GAGAS, and Yellow Book are all used interchangeably.

Beginning in the mid-1960s, both the number and the dollar amount of federal government programs and services increased substantially. This increase brought with it a demand for full accountability from those entrusted with public funds and the responsibility for managing government programs and services properly.

In 1969, the Comptroller General of the United States held a series of meetings with a group of state auditors and federal officials. These meetings identified a need to improve government auditing. One of the areas identified was the absence of formal GAS. In July 1969, the GAO initiated plans for an audit standards work group charged with the objective of developing GAS.

In 1970, the audit standards work group started the survey and research work on which the original 1972 Standards were based. The work group included representatives from the GAO, federal departments and agencies, state and local government auditors, and professional organizations including the AICPA. Assistance was also provided by academics and public interest groups. In June 1972, the Comptroller General issued the original version of the Yellow Book, entitled Standards for Audits of Governmental Organizations, Programs, Activities & Functions.

In 1979, the GAO started a project to revise the Standards. Based on comments and suggestions the GAO had received since the Standards were originally issued, a draft of proposed revised Standards was prepared and released for comment in August 1980. Comments received were analyzed and evaluated for appropriate consideration in arriving at the final draft Standards. The 1981 revision of GAGAS was signed by the Comptroller General on February 27, 1981.

In November 1985, the GAO started a project to clarify, update, and revise the 1981 revision of the Yellow Book. In December 1985, the Comptroller General appointed an Auditing Standards Advisory Council (ASAC) to advise him and the GAO on revising the Standards. The ASAC comprised members from federal, state, and local governments; public accounting; academia; and other special interest groups.

On March 16, 1987, an exposure draft (ED) was released for comment and was sent to audit officials at all levels of government and members of the public accounting profession, academia, professional organizations, and public interest groups. Comments received were analyzed and evaluated, and appropriate changes were made in the final draft. The final revised Standards were released in August 1988, superseding the 1981 revision.

In July 1993, an ED was released proposing changes to the 1988 Yellow Book revision. A revision, entitled Government Auditing Standards: 1994 Revision, was released on June 6, 1994. Its provisions were effective for financial audits of periods ending on or after January 1, 1995; and performance audits beginning on or after January 1, 1995.

After the issuance of the 1994 revision of the Yellow Book, three amendments were issued as follows:

Amendment No. 1: Documentation Requirements When Assessing Control Risk at Maximum for Controls Significantly Dependent Upon Computerized Information Systems, issued May 1999

Amendment No. 2: Auditor Communication, issued July 1999

Amendment No. 3: Independence, issued January 2002

In June 2003, the GAO released an omnibus revision to the Yellow Book. The standards became applicable for financial audits and attestation engagements of periods ending on or after January 1, 2004, and for performance audits beginning on or after January 1, 2004.

In July 2007, the GAO issued an omnibus revision to the Yellow Book. The 2007 Yellow Book became applicable for financial audits and attestation engagements for periods beginning on or after January 1, 2008, and for performance audits beginning on or after January 1, 2008.

In December 2011, the GAO issued the Government Auditing Standards (2011 Revision), which superseded the 2007 revision. The 2011 revision of GAS is currently effective.

In April 2017 GAO issued an exposure draft containing proposed changes to Government Auditing Standards, December 2011 Revision. When issued in final form the revision will supersede the December 2011 revision of the standards. The revision to Government Auditing Standards is not expected to be final until late 2017 or in 2018.

The proposed changes update the Yellow Book to reflect major developments since the last revision and to emphasize specific considerations applicable to the government environment. Among the changes are:

Next pageFont size:

Interval:

Bookmark:

Similar books «Yellow Book: Government Auditing Standards»

Look at similar books to Yellow Book: Government Auditing Standards. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Yellow Book: Government Auditing Standards and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.