Rodney Schulz - Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost

Here you can read online Rodney Schulz - Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2020, publisher: iUniverse, genre: Romance novel. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost

- Author:

- Publisher:iUniverse

- Genre:

- Year:2020

- Rating:4 / 5

- Favourites:Add to favourites

- Your mark:

Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Rodney Schulz: author's other books

Who wrote Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost? Find out the surname, the name of the author of the book and a list of all author's works by series.

Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

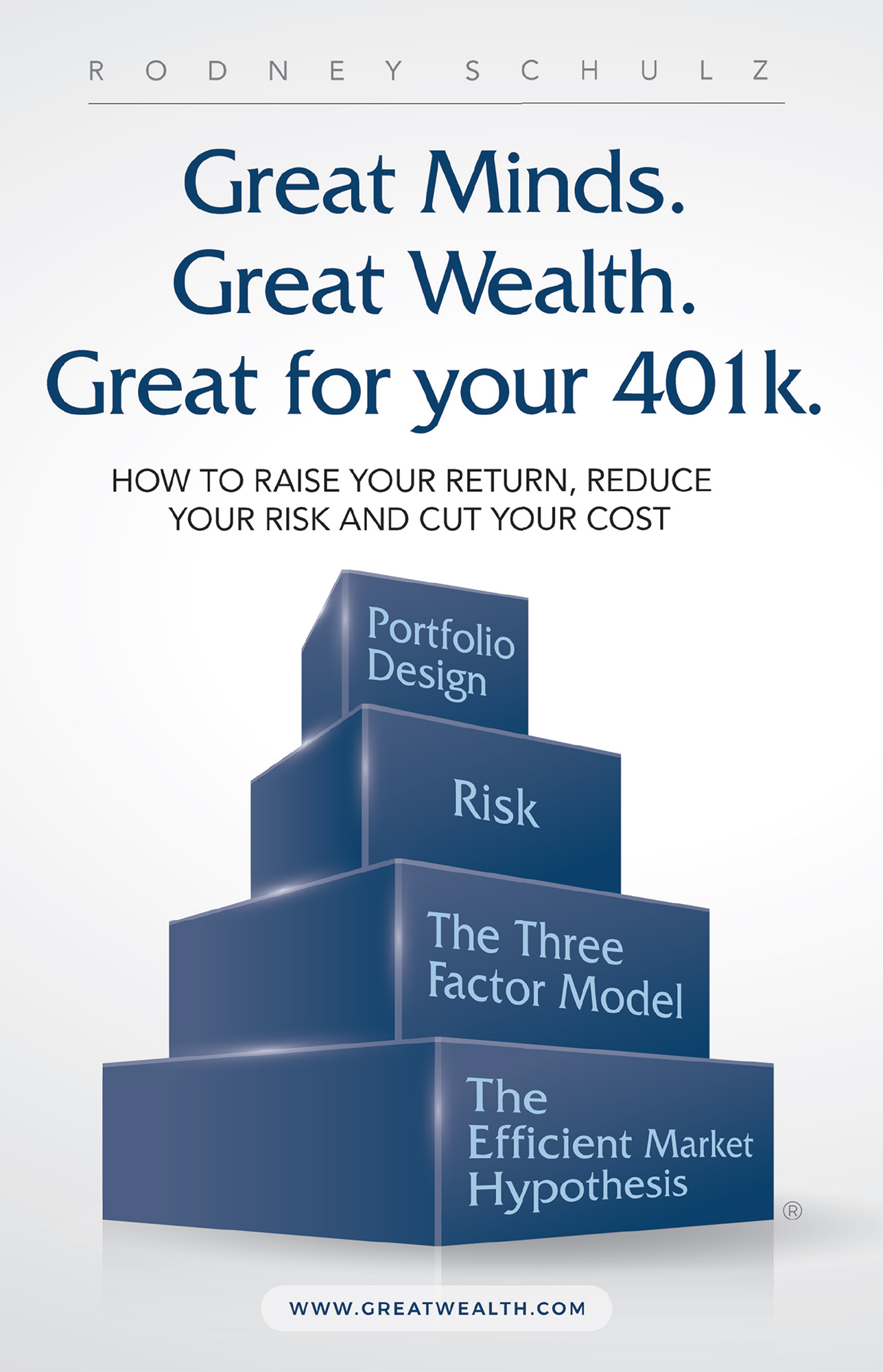

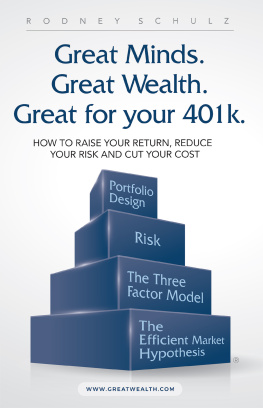

GREAT MINDS.

GREAT WEALTH.

GREAT FOR YOUR 401K.

HOW TO RAISE YOUR RETURN, REDUCE YOUR RISK AND CUT YOUR COST

RODNEY SCHULZ

Great Minds. Great Wealth. Great for Your 401k.

How to Raise Your Return, Reduce Your Risk and Cut Your Cost

Copyright 2020 Schulz Media LLC.

The Schulz Investment Pyramid used throughout this book is a registered trademark with the United States Patent and Trademark Office.

All rights reserved. No part of this book may be used or reproduced by any means, graphic, electronic, or mechanical, including photocopying, recording, taping or by any information storage retrieval system without the written permission of the author except in the case of brief quotations embodied in critical articles and reviews.

The information, ideas, and suggestions in this book are not intended to render professional advice. Before following any suggestions contained in this book, you should consult your personal accountant or other financial advisor. Neither the author nor the publisher shall be liable or responsible for any loss or damage allegedly arising as a consequence of your use or application of any information or suggestions in this book.

iUniverse

1663 Liberty Drive

Bloomington, IN 47403

www.iuniverse.com

1-800-Authors (1-800-288-4677)

Because of the dynamic nature of the Internet, any web addresses or links contained in this book may have changed since publication and may no longer be valid. The views expressed in this work are solely those of the author and do not necessarily reflect the views of the publisher, and the publisher hereby disclaims any responsibility for them.

Any people depicted in stock imagery provided by Getty Images are models, and such images are being used for illustrative purposes only.

Certain stock imagery Getty Images.

ISBN: 978-1-5320-6946-8 (sc)

ISBN: 978-1-5320-6944-4 (hc)

ISBN: 978-1-5320-6945-1 (e)

iUniverse rev. date: 03/16/2020

Contents

Whether youre a novice investor with a small portfolio or a seasoned investor sitting on millions of dollars, youre likely inundated with financial opinions. Unfortunately, when it comes to our personal wealth were all vulnerable to emotions. Therefore, most financial writers target emotions instead of explaining the facts in a way that is fun and interesting to read.

Nevertheless, there is hope and the cure is painless. In short, this book:

A. Presents an easy-to-understand, non-commercial, sound, concise body of pragmatic investment knowledge to help you; and

B. Does this in a way that is highly informative for the seasoned investor while not overwhelming to the novice investor.

Putting this information to work will allow you to:

1) Raise your return to ultimately make you wealt hier.

2) Reduce your risk to immediately decrease your investment heart burn.

3) Cut your cost so that you have more money to spend on the fun things of life .

An Added Bonus. Wouldnt you rather spend more time on the golf course, relaxing on the beach or enjoying your children and grandchildren? Enabling you to do this is another objective of this book, as most individuals have better things to do with their time than read and study mounds of information that has little or no value to their personal wealth. In fact, most investment news and information, if acted on, hurts, rather than helps, the investor. As you can see, this is a real win for you and those around you.

My Unique Position to Help You

Smart and well-educated finance professionals are a dime a dozen. Theyre everywhere, and investment books are ubiquitous.

The thing that makes this book different is my ability to decipher what really matters and put pragmatic Nobel Prize level financial knowledge in common terms for your application and benefit. This information will get you the maximum return for the amount of risk and cost. Moreover, it will help you understand and assess your risk while knowing the likely limits of your portfolio.

My Early Years. Unlike 99 percent of all top-tier MBAs (I got my MBA through the full time, day time program at Duke Universitys Fuqua School of Business), I grew up in a family where neither parent attended any college. My father was a blue-collar oil field worker and my mother drove a school bus. I honestly dont know if any of my grandparents even graduated from high school. My fathers father was a life-long farmer in central Kansas, while my mothers father spent his working life as a blue-collar worker in the oil fields of northeast Oklahoma and central Kansas.

No, my parents definitely werent stupid. However, I can still remember many typical family dinner conversations where Dad ranted about his frustration with engineers who dont have any common sense and my mother always being uneasy around people with money.

Nevertheless, I must have inherited some degree of cerebral capacity from them, as an engineering ability test I took in high school put my mechanical aptitude in the top 1 percent and my ACT math score was in the top 2 percent. Ten years later I scored a perfect 35/35 on the Analysis of Business Situations section of the Graduate Management Admissions Test (GMAT) and my combined math and English skills were in the top 4 percent of all college graduates. But again, and I truly mean this, smart and well-educated finance professionals are a dime a dozen.

After paying 100 percent of my way through a petroleum engineering degree at the University of Kansas I soon, like just about all engineers, found myself surrounded by other smart and well-educated people. As a young petroleum engineer I often worked on things as abstract as oil, gas and water flowing through the pores of rock thousands of feet underground. Another problem I worked on was to calculate the amount thousands of feet of steel pipe would stretch (due to weight, heat and external pressure) and shrink (due to internal pressure) when put in operation. I ran computer simulations on the above challenges, as well as many other situations. Things could get complicated quickly.

However, my ultimate job as a petroleum engineer was really quite simple:

1) How many dollars went into the hole?

2) What were the associated risks?

3) How many dollars would we likely get out of the hole?

This is very simple and very much like your financial situation; i.e.,

1) How many dollars should go into various segments of your portfolio?

2) What are the risks of each segment?

3) How much can you reasonably expect to get out of your portfolio over an unknown period of time?

In answering the three questions above concerning oil and gas situations countless times in just a few years, I realized there must be more to financial management than what I learned in one three-credit engineering economics course. Thus, I chose to invest much of what I had saved in five years of petroleum engineering work to finance an MBA from Duke Universitys Fuqua School of Business through their full-time, day-time program.

An Abrupt Turn of Ev ents

A few years after graduating from Duke my wife and I moved to Pittsburgh, PA, her hometown, for a variety of personal reasons. Not long thereafter, I found myself interviewing for the position of Financial Director/chief financial officer (CFO) for a 25-year-old college campus ministry organization with 150 employees in six states. Although it was a non-profit organization, we had a multi-million-dollar budget for operating expenses and a multi-million-dollar endowment fund invested in stocks and bonds.

To be sure, I really didnt want the position when I first interviewed for it. In fact, I went in to the interview hoping they would find someone else. But they made it clear: They wanted me. Their finance department was a mess (much more-so than they disclosed or anyone realized), and I had a track record of fixing things with an eye toward good financial management.

Next pageFont size:

Interval:

Bookmark:

Similar books «Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost»

Look at similar books to Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Great Minds. Great Wealth. Great for Your 401K.: How to Raise Your Return, Reduce Your Risk and Cut Your Cost and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.