James Gentle - Statistical Analysis of Financial Data: With Examples in R

Here you can read online James Gentle - Statistical Analysis of Financial Data: With Examples in R full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2020, publisher: CRC Press, genre: Science. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Statistical Analysis of Financial Data: With Examples in R

- Author:

- Publisher:CRC Press

- Genre:

- Year:2020

- Rating:4 / 5

- Favourites:Add to favourites

- Your mark:

Statistical Analysis of Financial Data: With Examples in R: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Statistical Analysis of Financial Data: With Examples in R" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Chapter 2 describes the methods of exploratory data analysis, especially graphical methods, and illustrates them on real financial data. Chapter 3 covers probability distributions useful in financial analysis, especially heavy-tailed distributions, and describes methods of computer simulation of financial data. Chapter 4 covers basic methods of statistical inference, especially the use of linear models in analysis, and Chapter 5 describes methods of time series with special emphasis on models and methods applicable to analysis of financial data.

Features

* Covers statistical methods for analyzing models appropriate for financial data, especially models with outliers or heavy-tailed distributions.

* Describes both the basics of R and advanced techniques useful in financial data analysis.

* Driven by real, current financial data, not just stale data deposited on some static website.

* Includes a large number of exercises, many requiring the use of open-source software to acquire real financial data from the internet and to analyze it.

James Gentle: author's other books

Who wrote Statistical Analysis of Financial Data: With Examples in R? Find out the surname, the name of the author of the book and a list of all author's works by series.

Statistical Analysis of Financial Data: With Examples in R — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Statistical Analysis of Financial Data: With Examples in R" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

CHAPMAN & HALL/CRC

Texts in Statistical Science Series

Joseph K. Blitzstein, Harvard University, USA

Julian J. Faraway, University of Bath, UK

Martin Tanner, Northwestern University, USA

Jim Zidek, University of British Columbia, Canada

Recently Published Titles

Theory of Spatial Statistics

A Concise Introduction

M.N.M van Lieshout

Bayesian Statistical Methods

Brian J. Reich and Sujit K. Ghosh

Sampling

Design and Analysis, Second Edition

Sharon L. Lohr

The Analysis of Time Series

An Introduction with R, Seventh Edition

Chris Chatfield and Haipeng Xing

Time Series

A Data Analysis Approach Using R

Robert H. Shumway and David S. Stoffer

Practical Multivariate Analysis, Sixth Edition

Abdelmonem Afifi, Susanne May, Robin A. Donatello, and Virginia A. Clark

Time Series: A First Course with Bootstrap Starter

Tucker S. McElroy and Dimitris N. Politis

Probability and Bayesian Modeling

Jim Albert and Jingchen Hu

Surrogates

Gaussian Process Modeling, Design, and Optimization for the Applied Sciences

Robert B. Gramacy

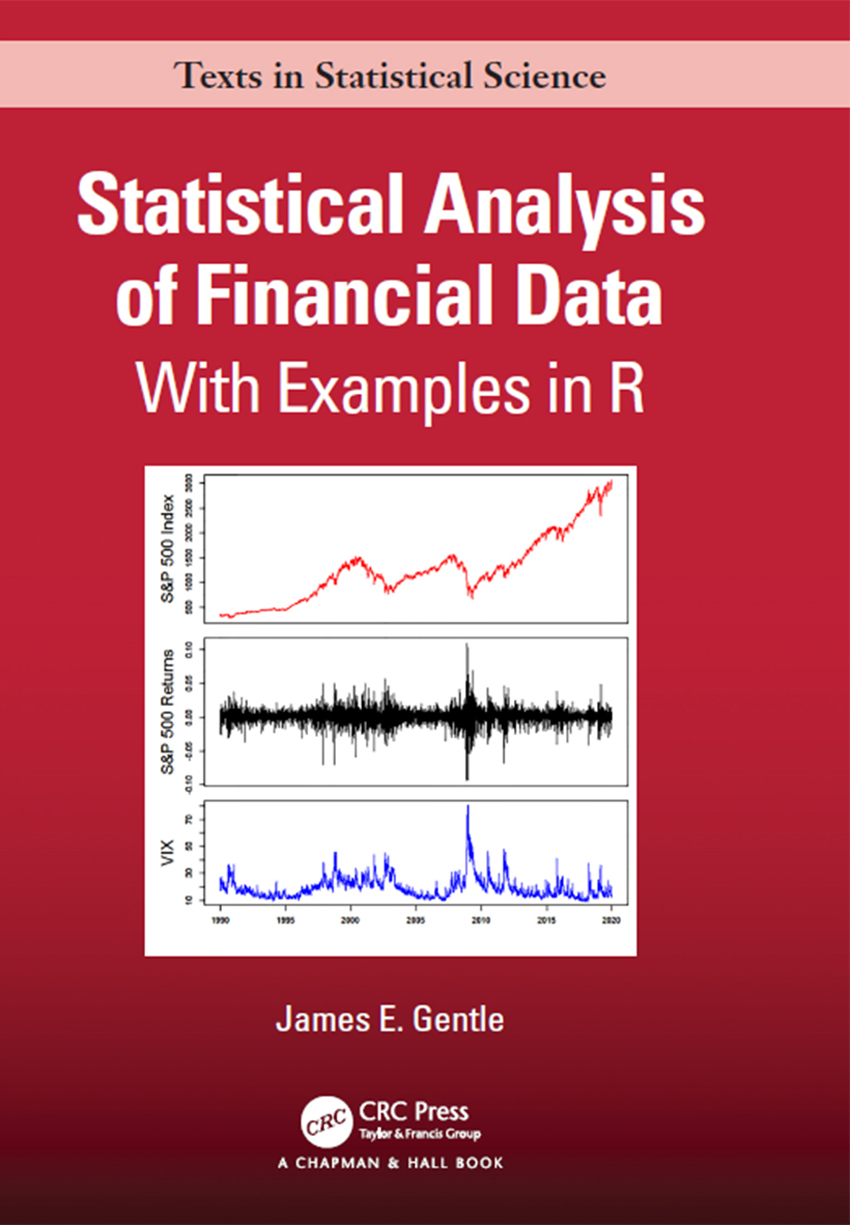

Statistical Analysis of Financial Data

With Examples in R

James E. Gentle

For more information about this series, please visit:

https://www.crcpress.com/ChapmanHallCRC-Texts-in-Statistical-Science/book-series/CHTEXSTASCI

James E. Gentle

First edition published 2020

by CRC Press

6000 Broken Sound Parkway NW, Suite 300, Boca Raton, FL 33487-2742

and by CRC Press

2 Park Square, Milton Park, Abingdon, Oxon, OX14 4RN

2020 Taylor & Francis Group, LLC

CRC Press is an imprint of Taylor & Francis Group, LLC

Reasonable efforts have been made to publish reliable data and information, but the author and publisher cannot assume responsibility for the validity of all materials or the consequences of their use. The authors and publishers have attempted to trace the copyright holders of all material reproduced in this publication and apologize to copyright holders if permission to publish in this form has not been obtained. If any copyright material has not been acknowledged please write and let us know so we may rectify in any future reprint.

Except as permitted under U.S. Copyright Law, no part of this book may be reprinted, reproduced, transmitted, or utilized in any form by any electronic, mechanical, or other means, now known or hereafter invented, including photocopying, microfilming, and recording, or in any information storage or retrieval system, without written permission from the publishers.

For permission to photocopy or use material electronically from this work, access

Trademark notice: Product or corporate names may be trademarks or registered trademarks, and are used only for identification and explanation without intent to infringe.

Library of Congress Cataloging-in-Publication Data

Library of Congress Control Number:2019956114

ISBN: 978-1-138-59949-9 (hbk)

ISBN: 978-0-429-48560-2 (ebk)

To Mara

This book is intended for persons with interest in analyzing financial data and with at least some knowledge of mathematics and statistics. No prior knowledge of finance is required, although a reader with experience in trading and in working with financial data may understand some of the discussion more readily. The reader with prior knowledge of finance may also come to appreciate some aspects of financial data from fresh perspectives that the book may provide. Financial data have many interesting properties, and a statistician may enjoy studying and analyzing the data just because of the challenges it presents.

There are many texts covering essentially the same material. This book differs from most academic texts because its perspective is that of a real-world trader who happens to be fascinated by data for its own sake. The emphasis in this book is on financial data. While some stale datasets at the books website are provided for examples of analysis, the book shows how and where to get current financial data, and how to model and analyze it.

Understanding financial data may increase ones success in the markets, but the book does not offer investment advice.

The organization and development of the book are data driven. The book begins with a general description of the data-generating processes that yield financial data. In the first chapter, many sets of data are explored statistically with little discussion of the statistical methods themselves, how these exploratory analyses were performed, or how the data were obtained. The emphasis is on the data-generating processes of finance: types of assets and markets, and how they function.

The first chapter may seem overly long, but I feel that it is important to have a general knowledge of the financial data-generating processes. A financial data analyst must not only know relevant statistical methods of analysis, the analyst must also know, for example, the difference between a seasoned corporate and a T-Bill, and must understand why returns in a short index ETF are positively correlated with the VIX.

While reading ?.

These questions are addressed in an appendix to , discusses computer methods used to obtain real financial data such as adjusted closing stock prices or T-Bill rates from the web, and to mung, plot, and analyze it.

The software used is R. Unless data can be obtained and put in a usable form, there can be no analysis. In the exercises for the appendix, the reader is invited to perform similar exploratory analyses of other financial data.

In the later chapters and associated exercises, the emphasis is on the methods of analysis of financial data. Specific datasets are used for illustration, but the reader is invited to perform similar analyses of other financial data.

I have expended considerable effort in attempting to make the Index complete and useful. The entries are a mix of terms relating to financial markets and terms relating to data science, statistics, and computer usage.

This book is about financial data and methods for analyzing it. Statisticians are fascinated by interesting data. Financial data is endlessly fascinating; it does not follow simple models. It is not predictable. There are no physical laws that govern it. It is big data. Perhaps best of all, an endless supply of it is available freely for the taking.

Access to financial data, and the financial markets themselves, was very different when I first began participating in the market over fifty years ago. There was considerably more trading friction then; commissions were very significant. The options markets for the retail investor/trader were almost nonexistent; there were no listed options (those came in 1973). Hedging opportunities were considerably more limited. There were no ETFs. (An early form was released in 1989, but died a year later; finally, the first Spider came out in 1993.) Most mutual funds were actively managed, and charged high fees.

Font size:

Interval:

Bookmark:

Similar books «Statistical Analysis of Financial Data: With Examples in R»

Look at similar books to Statistical Analysis of Financial Data: With Examples in R. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Statistical Analysis of Financial Data: With Examples in R and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.