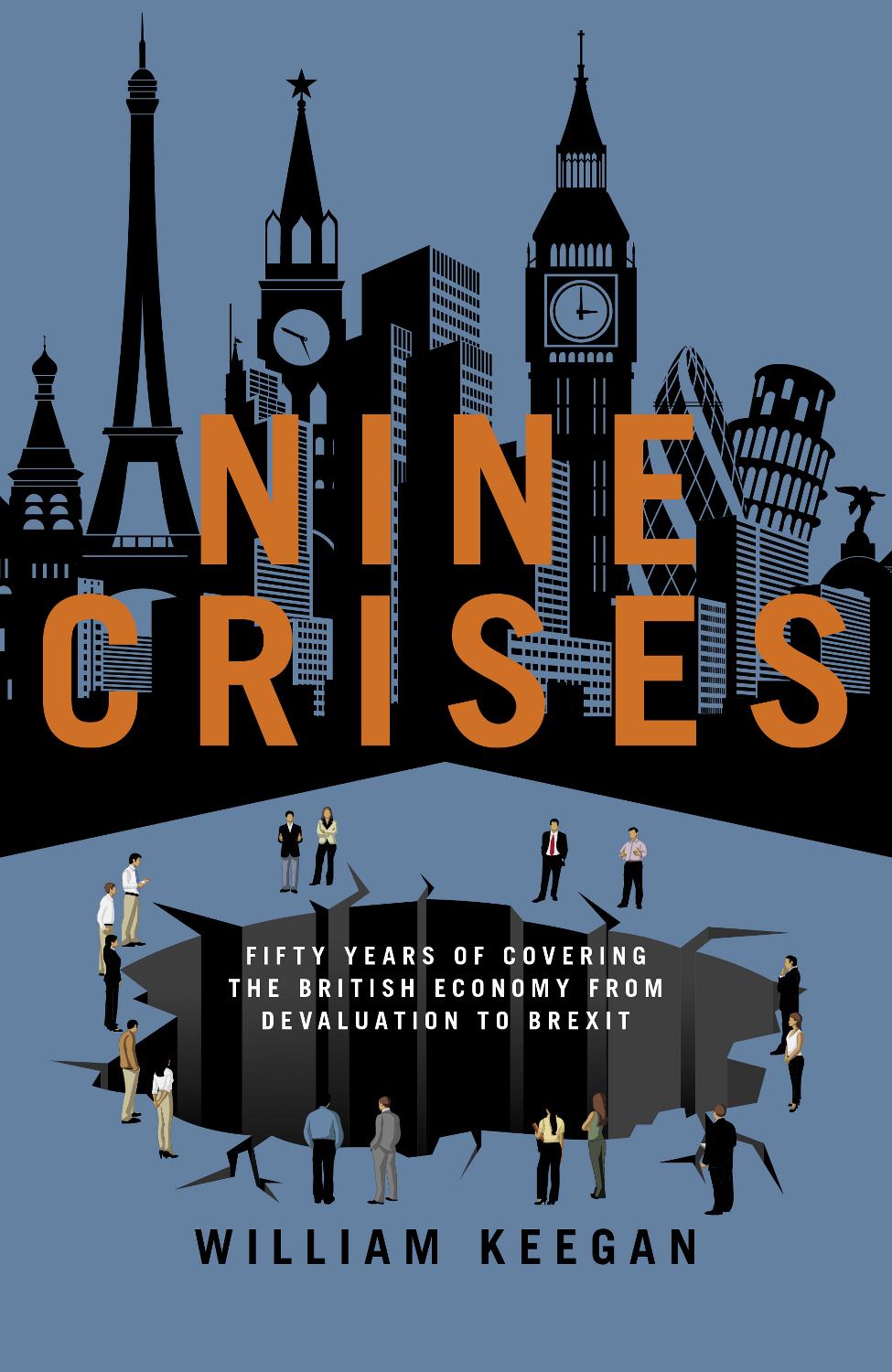

Keegan - Nine crises: fifty years of covering the British economy - from devaluation to Brexit

Here you can read online Keegan - Nine crises: fifty years of covering the British economy - from devaluation to Brexit full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. City: Great Britain, year: 2019, publisher: Biteback Publishing, genre: Science. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

Nine crises: fifty years of covering the British economy - from devaluation to Brexit: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Nine crises: fifty years of covering the British economy - from devaluation to Brexit" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

A collapsing pound, spiralling oil prices, near-rationing of electricity... over the past half-century, Britains economy has lurched from one crisis to another, though it somehow always survives or at least it has done until now.

Veteran financial journalist William Keegan has seen it all, from the 1967 devaluation to the three-day week, from Black Wednesday to the global financial crash of 2007-08. In a career that has seen him hop from Fleet Street to the Old Lady of Threadneedle Street and back again, he has nurtured connections with Chancellors of the Exchequer, Governors of the Bank of England, influential economists and Fleet Street legends.

Now, in this lively and wide-ranging account, he takes us on a tumultuous journey through the past fifty years of our economic history and looks ahead to explain why Brexit poses the biggest existential threat the British economy has yet faced.

Peppered with anecdotes and memories from the authors illustrious...

Keegan: author's other books

Who wrote Nine crises: fifty years of covering the British economy - from devaluation to Brexit? Find out the surname, the name of the author of the book and a list of all author's works by series.

Nine crises: fifty years of covering the British economy - from devaluation to Brexit — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Nine crises: fifty years of covering the British economy - from devaluation to Brexit" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

To my wife, Hilary Stonefrost, and my children

M y interest in the economy was aroused partly by a desire to understand the political debate and partly by a distaste for translating Greek and Latin texts. The time was the 1950s. The newspapers were full of news of Britains economic problems plus a change and I wanted to understand what I read in the papers or, at least, to understand more.

The connection with Greek and Latin texts was this: I had been a member of the Classical Sixth at my grammar school, Wimbledon College, and had been accepted to read the Classical Tripos at Trinity College, Cambridge. But, while I have been ever grateful to those Jesuits at Wimbledon for introducing me to or foisting upon me classical literature, and although I appreciated the prose and the poetry, I struggled with translation. In particular, composing Greek and Latin verse which one was required to do in those days was definitely not for me. Moreover, I knew in my heart of hearts that what had got me into Cambridge was not my Greek or Latin, but ancient history.

Indeed, history is my favourite subject. It embraces everything which philosophy did in Ancient Greece. But just as I did not wish to ruin my love of English literature by reading it as a discipline, I felt that I could study history for the rest of my life, whereas, if I did not have a go at economics, I probably never would.

In those far-off days of the 1950s, the male youth of the nation, if pronounced medically fit, were required to do two years National Service, in the army, navy or air force. While I was doing my basic training at Catterick Camp, Yorkshire, in the 5th Royal Tank Regiment, I attended an evening course of lectures on economics given by an economist from Hull University. I duly took notes, but by the evening, a day of intense drill on the parade ground had taken its toll, and I fear that not much of what I heard sank in. I became aware of this with a vengeance many years later, when I came across my notebook for that course. This was well after I had left Cambridge. It was clear that the lectures by the academic from Hull had been first rate. But sink in they had not. An embarrassing illustration of my economic ignorance at the time and, it has to be said, of everybody else present on the occasion was provided during a casual discussion in the officers mess at HQ Northern Ireland Command, where I was posted in 195859.

A certain captain opined, If the economy is in such a state, why dont they just print more money? Yes, we all seemed to think, just give us more money and we wont feel so broke.

Now, little did those present know it, but we had stumbled upon one of the burning issues of macroeconomic policy, which was being debated at a high level at the time and has been furiously debated ever since.

Money has to be backed by real goods and services. One of the favourite questions asked of fresh students of economics is: what would happen if you doubled the money supply? (Or, more strictly, the stock of money.) The short answer is that unless this were to be accompanied by a doubling of output of goods and services, there would be a doubling of the price level too much money chasing too few goods.

Nevertheless, those officers in HQ Northern Ireland Command may have had a naive view of the economic problem I know I certainly did but what successive governments and Treasury and Bank of England officials were struggling with then, and have been struggling with ever since, is the question of how to conduct economic policy so as to achieve an optimal balance between movements in output, employment and inflation.

The officers mess just print more money school does not seem so naive if the economy is heavily depressed and machines, service equipment and above all people are lying idle when there is latent demand for the goods and services they are potentially able to produce. More money, via increases in government spending, tax cuts or lower interest rates, is just what is required in such circumstances, as was vividly demonstrated during the Great Recession of 200809, which was induced primarily by the world financial crisis.

Nevertheless, steering the economy is not that simple, as I was to discover from my economics supervisors and lecturers at Cambridge, and during my subsequent career in financial journalism.

I confess that there are many aspects of economics that do not appeal to me. My interest has always been in political economy, the relationship between economics and politics, and the discussions and battles that go on in public and private between economists and policymakers. This involves a close study of the relationships between the most senior people responsible for economic policy decisions namely, the Prime Minister (who is also, after all, the First Lord of the Treasury), the Chancellor and the Governor of the Bank of England, and their advisers.

These men or women may be ultimately responsible for the big economic policy decisions in our democracy with the approval, if they deign to seek it, of Parliament but they are only in charge up to a point. They are, as former Prime Minister Harold Macmillan once said, at the mercy of events. Macmillan, when asked what he feared most, replied: The opposition of events. This subsequently became The opposition of events, dear boy, events. The dear boy was apparently not actually said by Macmillan, but it did sound like him. Such great remarks become clichs for a good reason. They strike a chord. His comment was also a dig at the weakness of the opposition.

Events can include the impact of wars or other military operations Suez in 1956; the Falklands in 1982 and what economists call shocks: the two oil crises of the 1970s; the unexpected financial crash of 200709; and, more recently, Brexit.

The Queen, not known for her views on economic policy, became celebrated in November 2008 for her observation about the unanticipated nature of the crash. Why, she asked, when opening a new wing of the London School of Economics, did nobody notice it?

This gave me a golden opportunity when, shortly afterwards, I was awarded the CBE and found myself in front of the monarch, who looked at me and said, And what do you do?

I write about the economy for The Observer newspaper, I replied. There was a brief silence. Then I added, I was one of the people who didnt warn you.

B efore I embarked on economics, I had a brief brush with the law. I read part of a book by a distinguished academic lawyer, Glanville Williams, but could rustle up little enthusiasm for the subject. My memory, probably distorted, is that at some stage close to page 90 the author suggests that if by now the reader is bored, he should certainly not contemplate reading law.

This was during the year I spent teaching, between the end of my National Service in 1959 and going up to Cambridge in October 1960. It was during a spell teaching English in La Tour-de-Peilz, near Vevey, Switzerland, that I met another prospective Cambridge undergraduate, David Simons, who was working as a stageur at the Nestl headquarters there.

David told me that the American (strictly, Canadian) economist J. K. Galbraith had come down from the Swiss mountains to give a lecture, and how impressive he was. Not only was Galbraith 6ft 8in. tall; he had written a book, The Affluent Society, which was seriously critical of the conventional economics that I was about to study.

There was no shortage of affluence in the Vevey region at the time. Among the local residents we were to see at the expats favourite caf (Les Trois Rois, long since transformed into a bank) were Charlie Chaplin, Peter Ustinov and Van Johnson. Vladimir Nabokov lived in Montreux. But the affluent society Galbraith was writing about was the USA, about which he made his celebrated criticism of the contrast between private opulence and public squalor.

Font size:

Interval:

Bookmark:

Similar books «Nine crises: fifty years of covering the British economy - from devaluation to Brexit»

Look at similar books to Nine crises: fifty years of covering the British economy - from devaluation to Brexit. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Nine crises: fifty years of covering the British economy - from devaluation to Brexit and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.