Your Money and Your Brain

How the New Science of Neuroeconomics Can Help Make You Rich

Jason Zweig

Simon & Schuster

New York London Toronto Sydney

SIMON & SCHUSTERRockefeller Center1230 Avenue of the AmericasNew York, NY 10020Copyright 2007 by Jason ZweigAll rights reserved, including the right of reproduction in whole or in part in any form.SIMON & SCHUSTER and colophon are registered trademarks of Simon & Schuster, Inc.Zweig, Jason.Your money and your brain: how the new science of neuroeconomics can help make you rich / Jason Zweig.p. cm.Includes bibliographic references.1. InvestmentsPsychological aspects. 2. FinanceDecision making. 3. Neuroeconomics.HG4515.15.Z84 2007332.601'9dc22 2006100986ISBN-13: 978-1-4165-3979-7ISBN-10: 1-4165-3979-4Visit us on the World Wide Web:http://www.SimonSays.com

For my wife, who did the real work with love and grace

Contents

Chapter One

Neuroeconomics

Chapter Two

"Thinking" and "Feeling"

Chapter Three

Greed

Chapter Four

Prediction

Chapter Five

Confidence

Chapter Six

Risk

Chapter Seven

Fear

Chapter Eight

Surprise

Chapter Nine

Regret

Chapter Ten

Happiness

CHAPTER ONE

Neuroeconomics

BRAIN, n. An apparatus with which we think that we think.

Ambrose Bierce

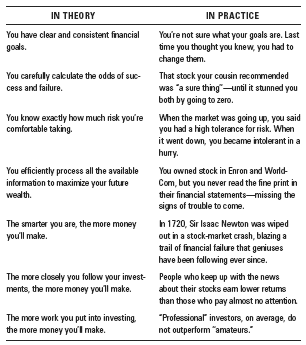

"HOW COULD I HAVE BEEN SUCH AN IDIOT?" IF YOU'VE never yelled that sentence at yourself in a fury, you're not an investor. There may be nothing across the entire spectrum of human endeavor that makes so many smart people feel so stupid as investing does. That's why I've set out to explain, in terms any investor can understand, what goes on inside your brain when you make decisions about money. To get the best use out of any tool or machine, it helps to know at least a little about how it works; you will never maximize your wealth unless you can optimize your mind. Fortunately, over the past few years, scientists have made stunning discoveries about the ways the human brain evaluates rewards, sizes up risks, and calculates probabilities. With the wonders of imaging technology, we can now observe the precise neural circuitry that switches on and off in your brain when you invest.I've been a financial journalist since 1987, and nothing I've ever learned about investing has excited me more than the spectacular findings emerging from the study of "neuroeconomics." Thanks to this newborn fielda hybrid of neuroscience, economics, and psychologywe can begin to understand what drives investing behavior not only on the theoretical or practical level, but as a basic biological function. These flashes of fundamental insight will enable you to see as never before what makes you tick as an investor.On this ultimate quest for financial self-knowledge, I'll take you inside laboratories run by some of the world's leading neuroeconomists and describe their fascinating experiments firsthand, since I've had my own 1 brain studied again and again by these researchers. (The scientific consensus on my cranium is simple: It's a mess in there.)The newest findings in neuroeconomics suggest that much of what we've been told about investing is wrong. In theory, the more we learn about our investments, and the harder we work at understanding them, the more money we will make. Economists have long insisted that investors know what they want, understand the tradeoff between risk and reward, and use information logically to pursue their goals.In practice, however, those assumptions often turn out to be dead wrong. Which side of this table sounds more like you?

You're not alone. Like dieters lurching from Pritikin to Atkins to South Beach and ending up at least as heavy as they started, investors habitually are their own worst enemies, even when they know better.Everyone knows that you should buy low and sell highand yet, all too often, we buy high and sell low.Everyone knows that beating the market is nearly impossiblebut just about everyone thinks he can do it.Everyone knows that panic selling is a bad ideabut a company that announces it earned 23 cents per share instead of 24 cents can lose $5 billion of market value in a minute-and-a-half.Everyone knows that Wall Street strategists can't predict what the market is about to dobut investors still hang on every word from the financial pundits who prognosticate on TV.Everyone knows that chasing hot stocks or mutual funds is a sure way to get burnedyet millions of investors flock back to the flame every year. Many do so even though they swore, just a year or two before, never to get burned again.One of the themes of this book is that our investing brains often drive us to do things that make no logical sensebut make perfect emotional sense. That does not make us irrational. It makes us human. Our brains were originally designed to get more of whatever would improve our odds of survival and to avoid whatever would worsen the odds. Emotional circuits deep in our brains make us instinctively crave whatever feels likely to be rewardingand shun whatever seems liable to be risky.To counteract these impulses from cells that originally developed tens of millions of years ago, your brain has only a thin veneer of relatively modern, analytical circuits that are often no match for the blunt emotional power of the most ancient parts of your mind. That's why knowing the right answer, and doing the right thing, are very different.An investor I'll call "Ed," a real estate executive in Greensboro, North Carolina, has rolled the dice on one high-tech and biotech company after another. At last count, Ed had lost more than 90% of his investment on at least four of these stocks. After Ed had lost 50% of his money, "I swore I'd sell if they fell another 10%," he recalls. "When they still kept dropping, I kept dropping my selling point instead of getting out. It felt like the only thing worse than losing all that money on paper would be selling and losing it for real." His accountant has reminded him that if he sells, he can write off the losses and cut his income tax billbut Ed still can't bear to do it. "What if they go up from here?" he asks plaintively. "Then I'd feel stupid

twiceonce for buying them and once for selling them."In the 1950s, a young researcher at the RAND Corporation was pondering how much of his retirement fund to allocate to stocks and how much to bonds. An expert in linear programming, he knew that "I should have computed the historical co-variances of the asset classes and drawn an efficient frontier. Instead, I visualized my grief if the stock market went way up and I wasn't in itor if it went way down and I was completely in it. My intention was to minimize my future regret. So I split my contributions 50/50 between bonds and equities." The researcher's name was Harry M. Markowitz. Several years earlier, he had written an article called "Portfolio Selection" for the

Journal of Finance showing exactly how to calculate the tradeoff between risk and return. In 1990, Markowitz shared the Nobel Prize in economics, largely for the mathematical breakthrough that he had been incapable of applying to his own portfolio.Jack and Anna Hurst, a retired military officer and his wife who live near Atlanta, seem like very conservative investors. They have no credit card debt and keep almost all of their money in dividend-paying, blue-chip stocks. But Hurst also has what he calls a "play" account, in which he takes big gambles with small amounts of money. Betting on a few long shots in the stock market is Hurst's way of trying to fund what he calls his "lottery dreams." Those dreams are important to Hurst, because he has amyotrophic lateral sclerosis (ALS, or Lou Gehrig's disease); he's been completely paralyzed since 1989. Hurst can invest only by operating a laptop computer with a special switch that reads the electrical signals in his facial muscles. In 2004, one of his "lottery" picks was Sirius Satellite Radio, one of the most volatile stocks in America. Hurst's dreams are to buy a Winnebago customized for quadriplegics and to finance an "ALS house" where patients and their families can get special care. He is both a conservative

Next page