Matt Bamber - Accounting and Finance for Managers. A Decision-Making Approach

Here you can read online Matt Bamber - Accounting and Finance for Managers. A Decision-Making Approach full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2014, publisher: Kogan Page Publishers;Kogan Page, genre: Home and family. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Accounting and Finance for Managers. A Decision-Making Approach

- Author:

- Publisher:Kogan Page Publishers;Kogan Page

- Genre:

- Year:2014

- Rating:5 / 5

- Favourites:Add to favourites

- Your mark:

Accounting and Finance for Managers. A Decision-Making Approach: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Accounting and Finance for Managers. A Decision-Making Approach" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Accounting and Finance for Managers is a new text specifically designed to improve analytical skills and help readers use accounting and finance tools for managerial advantage.

Ideal for self study as well as classroom learning, it includes worked examples throughout the chapters as well as real-world scenarios and full exercises at the end of each chapter. Providing coverage of basic bookkeeping, readers will learn how to interpret financial statements and grasp underlying theory, interpret a cash budget and identify potential problems, identify appropriate pricing strategies to fit different markets and products/services and incorporate financial evaluation into operational decision making and problem solving.

With full supporting resources including lecture slides for each chapter and a breakdown of how each chapter relates to course structures, Accounting and Finance for Managers is essential reading for any student or manager.

Matt Bamber: author's other books

Who wrote Accounting and Finance for Managers. A Decision-Making Approach? Find out the surname, the name of the author of the book and a list of all author's works by series.

Accounting and Finance for Managers. A Decision-Making Approach — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Accounting and Finance for Managers. A Decision-Making Approach" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

D ouble-entry bookkeeping (bookkeeping, for short) is best taught through t-accounts; named thus because of their shape. T-accounts have a left side and a right side. Hereafter these will be referred to as the DEBIT side and the CREDIT side. This links back to the golden rule of accounting: that every debit must have an equal and opposite credit otherwise your ledgers would not balance.

Over the next few pages we will walk you through each of the Mobius Inc examples, completing the t-accounts as we go.

Bookkeeping comes naturally to a small number of people, but to the majority, however, this is something which needs to be practised and given careful consideration. Regardless of whether you get it within five minutes or five years, for almost everyone there is a light-bulb moment where everything clicks into place and you reflect uncomprehendingly on the times you couldnt see how it worked.

Approaching double-entry bookkeeping

Step 1: Set up your t-accounts

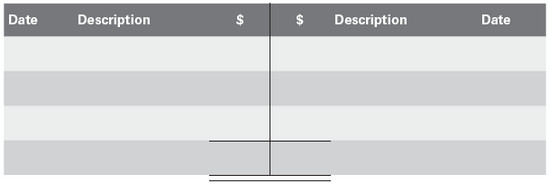

A t-account captures the key information about a transaction:

- the date;

- an outline description of the transaction;

note that this is normally the name of the account the other side of the journal entry is going to;

- the value.

For example, our first transaction involves two t-accounts: cash at bank and in hand; and share capital. The cash at bank and in hand t-account would appear as shown in .

Table A.1 Cash at bank and in hand

Note that there the $ or value columns need to be totalled. That is because each t-account needs to balance out at the end of the period of account:

- On the one hand, statement of financial position balances, for example cash at bank and in hand dont stop existing at the end of a period and therefore the amounts left over can be carried forward to the next period.

- On the other hand, income statement accounts, for example rental costs, relate to a period of account and once they have been incurred and paid, they should be closed out.

More on this later

Step 2: Write out your journal entry

Certainly, while youre in the initial learning stages of bookkeeping it is good practice to write out every journal entry. As you progress, you might stop doing this. Note, however, that if you dont write out the entry in full and you make an error (eg a transposition error, post two debits instead of a debit and credit, miss one side of the transaction), tracing the error back is more difficult.

The question states:

Mobius Inc (1)

On day 1, you opt to put financial distance between you and the trading entity and transfer $1,000 from your personal bank account to a bank account you hold in the name of the new enterprise Mobius Inc.

The journal entry is as follows:

$ | $ | |

Debit | Cash at bank and in hand | 1,000 |

Credit | Share capital: equity and reserves | 1,000 |

Useful tip

People who struggle with double-entry bookkeeping often dont understand the relevance of posting an entry as either a debit or a credit. The interconnectedness of position and performance provides the clue that we need. The grid below might help you to understand.

First, however, remember the accounting equation:

Assets MINUS Liabilities EQUALS Equity + Reserves

(Assets Liabilities = Equity and Reserves)

For this equation to work, an increase in assets would necessarily lead to either:

- a decrease in another asset;

- an increase in liabilities; or

- an increase in equity and reserves.

Examples might be:

- a decrease in another asset, eg swapping cash for inventory;

- an increase in liabilities, eg buying inventory on credit from a supplier;

- an increase in equity and reserves, eg selling share capital for cash.

To continue

We know that the profit is taken to equity and reserves to close it out at the end of a period. A simple double entry effecting both the statement of financial position and income statement (ie performance and position) might be:

- An operating expense being paid, eg rent.

- Cash would reduce (decrease in assets) and the rental cost in the income statement would increase.

Assuming this was the only transaction a business undertook during the period of account, at the end of the year this rental expense would be the loss for the period. This balance would be taken to retained earnings (a sub-heading under reserves).

Therefore, our accounting equation holds: a decrease in assets is offset by a decrease in equity and reserves.

The accounting equation tells us that there are two equal and opposite sides to every transaction. This can be summarized as shown in .

Table A.2

Debit | Credit | |

Assets and liabilities (excluding equity and reserves) | Assets increase Liabilities decrease (ie positive effect on financial position) | Assets decrease Liabilities increase (ie negative effect on financial position) |

Income statement and Equity and reserves | Expenses increase (Revenue decreases) (ie negative impact on performance; reduce profit) Equity and reserves decrease | Expenses decrease (Revenue increases) (ie positive impact on performance; increase profit) Equity and reserves increase |

Or, in shorthand ().

Table A.3

Debit | Credit |

Assets and liabilities (excluding equity and reserves) | + |

Income statement and Equity and reserves | + |

)

Table A.4

Cash at bank and in hand | |||||

Date | Description | $ | $ | Description | Date |

Day 1 | Initial investment capital | 1,000 | |||

Share capital | |||||

Date | Description | $ | $ | Description | Date |

1,000 | Bank | Day 1 |

Step 4: Close out the t-accounts

Assuming that this is the only transaction, you now need to move your closing balances to a trial balance and then into the financial statements ().

Table A.5

Cash at bank and in hand | |||||

Date | Description | $ | $ | Description | Date |

Beginning of day 1 | Balance brought forward | ||||

Day 1 | Initial investment capital | 1,000 | |||

1,000 | Balance carried forward | End of day 1 | |||

1,000 | 1,000 | ||||

Beginning of day 2 | Balance brought forward | 1,000 | |||

Share capital | |||||

Date | Description | $ | $ | Description | Date |

Balance brought forward | Beginning of day 1 | ||||

1,000 | Bank | Day 1 | |||

End of day 1 | Balance carried forward |

Font size:

Interval:

Bookmark:

Similar books «Accounting and Finance for Managers. A Decision-Making Approach»

Look at similar books to Accounting and Finance for Managers. A Decision-Making Approach. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Accounting and Finance for Managers. A Decision-Making Approach and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.