Simão Moraes Sarmento - A Machine Learning based Pairs Trading Investment Strategy

Here you can read online Simão Moraes Sarmento - A Machine Learning based Pairs Trading Investment Strategy full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2020, publisher: Springer, genre: Romance novel. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:A Machine Learning based Pairs Trading Investment Strategy

- Author:

- Publisher:Springer

- Genre:

- Year:2020

- Rating:5 / 5

- Favourites:Add to favourites

- Your mark:

A Machine Learning based Pairs Trading Investment Strategy: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "A Machine Learning based Pairs Trading Investment Strategy" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

This book investigates the application of promising machine learning techniques to address two problems: (i) how to find profitable pairs while constraining the search space and (ii) how to avoid long decline periods due to prolonged divergent pairs. It also proposes the integration of an unsupervised learning algorithm, OPTICS, to handle problem (i), and demonstrates that the suggested technique can outperform the common pairs search methods, achieving an average portfolio Sharpe ratio of 3.79, in comparison to 3.58 and 2.59 obtained using standard approaches. For problem (ii), the authors introduce a forecasting-based trading model capable of reducing the periods of portfolio decline by 75%. However, this comes at the expense of decreasing overall profitability. The authors also test the proposed strategy using an ARMA model, an LSTM and an LSTM encoder-decoder.

Simão Moraes Sarmento: author's other books

Who wrote A Machine Learning based Pairs Trading Investment Strategy? Find out the surname, the name of the author of the book and a list of all author's works by series.

A Machine Learning based Pairs Trading Investment Strategy — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "A Machine Learning based Pairs Trading Investment Strategy" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

SpringerBriefs present concise summaries of cutting-edge research and practical applications across a wide spectrum of fields. Featuring compact volumes of 50 to 125 pages, the series covers a range of content from professional to academic.

More information about this subseries at http://www.springer.com/series/10618 Typical publications can be:

A timely report of state-of-the art methods

An introduction to or a manual for the application of mathematical or computer techniques

A bridge between new research results, as published in journal articles

A snapshot of a hot or emerging topic

An in-depth case study

A presentation of core concepts that students must understand in order to make independent contributions

SpringerBriefs are characterized by fast, global electronic dissemination, standard publishing contracts, standardized manuscript preparation and formatting guidelines, and expedited production schedules.

On the one hand,SpringerBriefs in Applied Sciences and Technology are devoted to the publication of fundamentals and applications within the different classical engineering disciplines as well as in interdisciplinary fields that recently emerged between these areas. On the other hand, as the boundary separating fundamental research and applied technology is more and more dissolving, this series is particularly open to trans-disciplinary topics between fundamental science and engineering.

Indexed by EI-Compendex, SCOPUS and Springerlink.

This Springer imprint is published by the registered company Springer Nature Switzerland AG

The registered company address is: Gewerbestrasse 11, 6330 Cham, Switzerland

Augmented Dickey-Fuller

ANNArtificial neural network

ARMAAutoregressivemoving-average

DBSCANDensity-based spatial clustering of applications with noise

ETFExchange-traded fund

FNNFeedforward neural network

GARCHGeneralized autoregressive conditional heteroskedasticity

LSTMLong short-term memory

MAEMean absolute error

MDDMaximum drawdowm

MLPMultilayer perceptron

MSEMean squared error

OPTICSOrdering points to identify the clustering structure

PCAPrincipal component analysis

RNNRecurrent neural network

ROIReturn on investment

SRSharpe ratio

SSDSum of Euclidean squared distance

t-SNET-distributed Stochastic Neighbor Embedding

Pairs Trading is a well-known investment strategy developed in the 1980s. It has been employed as one important long/short equity investment tool by hedge funds and institutional investors Cavalcante et al. [

Once the pairs have been identified, the investor may proceed with the strategys second step. The underlying premise is that if two securities price series have been moving close in the past, then this should persist in the future. Therefore, if an irregularity occurs, it should provide an interesting trade opportunity to profit from its correction. To find such opportunities, the spread between the two constituents of the pairs must be continuously monitored. When a statistical anomaly is detected, a market position is entered. The position is exited upon an eventual spread correction. It is interesting to observe that this strategy relies on the relative value of two securities, regardless of their absolute value.

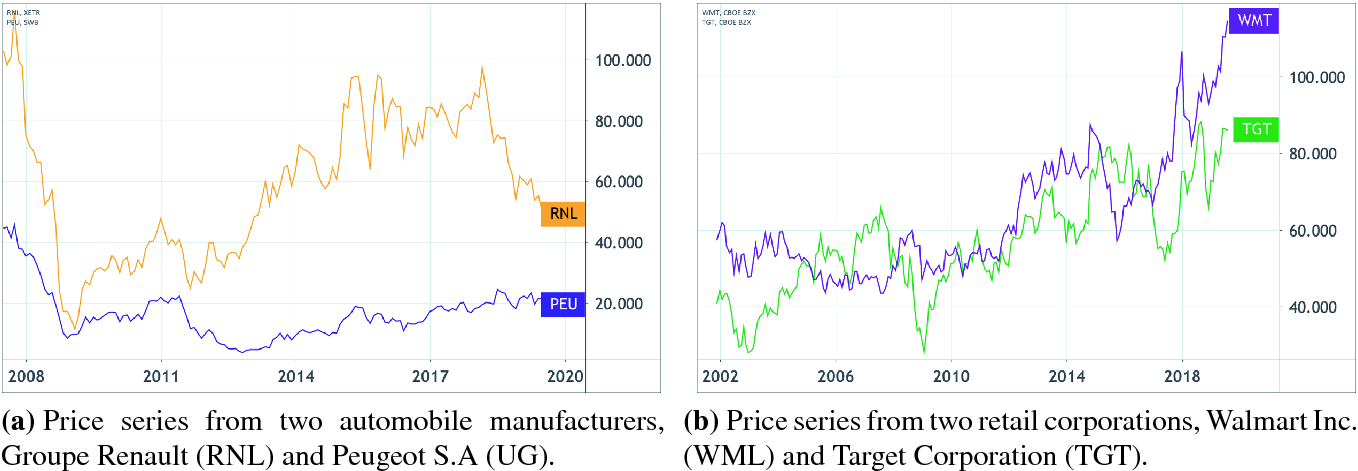

Price series which could potentially form profitable pairs

Font size:

Interval:

Bookmark:

Similar books «A Machine Learning based Pairs Trading Investment Strategy»

Look at similar books to A Machine Learning based Pairs Trading Investment Strategy. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book A Machine Learning based Pairs Trading Investment Strategy and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.