Ray LeVitre - 20 retirement decisions you need to make right now

Here you can read online Ray LeVitre - 20 retirement decisions you need to make right now full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2010, publisher: Sphinx Publishing, genre: Romance novel. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:20 retirement decisions you need to make right now

- Author:

- Publisher:Sphinx Publishing

- Genre:

- Year:2010

- Rating:4 / 5

- Favourites:Add to favourites

- Your mark:

20 retirement decisions you need to make right now: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "20 retirement decisions you need to make right now" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Ray LeVitre: author's other books

Who wrote 20 retirement decisions you need to make right now? Find out the surname, the name of the author of the book and a list of all author's works by series.

20 retirement decisions you need to make right now — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "20 retirement decisions you need to make right now" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Copyright 2010 by Ray E. LeVitre

Cover and internal design 2010 by Sourcebooks, Inc.

Cover design by KT Design

Cover image Comstock/Jupiter Images

Sourcebooks and the colophon are registered trademarks of Sourcebooks, Inc.

All rights reserved. No part of this book may be reproduced in any form or by any electronic or mechanical means including information storage and retrieval systemsexcept in the case of brief quotations embodied in critical articles or reviewswithout permission in writing from its publisher, Sourcebooks, Inc.

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.From a Declaration of Principles Jointly Adopted by a Committee of the American BarAssociation and a Committee of Publishers and Associations

All brand names and product names used in this book are trademarks, registered trademarks, or trade names of their respective holders. Sourcebooks, Inc., is not associated with any product or vendor in this book.

Visit www.networthadvice.com for updated charts.

First edition: 2003

Published by Sphinx Publishing, an imprint of Sourcebooks, Inc.

P.O. Box 4410, Naperville, Illinois 60567-4410

(630) 961-3900

Fax: (630) 961-2168

www.sourcebooks.com

Library of Congress Cataloging-in-Publication data is on file with the publisher.

Printed and bound in the United States of America.

VP 10 9 8 7 6 5 4 3 2 1

To the awesome women in my life

My wife, Jana, and my daughters, Brianna and Alexis

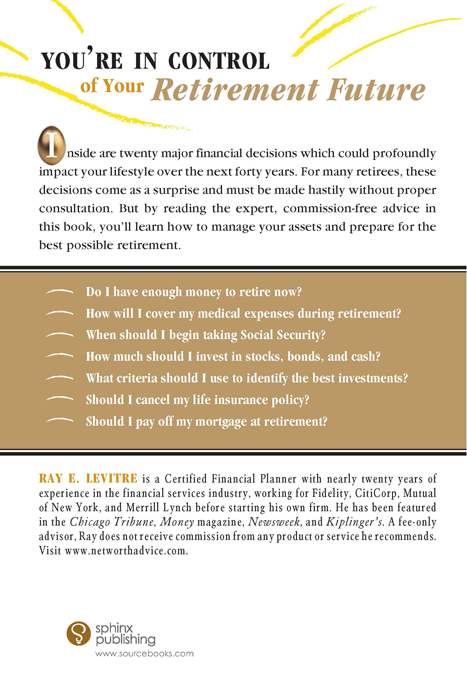

R ay E. LeVitre is a fee-only Certified Financial Planner who specializes in helping people develop and manage their financial plans at and through retirement. Ray has seen all sides of the financial services industry. Early in his career he spent time at Fidelity Investments, Citicorp, and Mutual of New York and later went on to build a career at Merrill Lynch working as a financial consultant and branch manager. Ray now runs an independent fee-only financial planning practice. He has been retained by many Fortune 500 companies to teach financial management seminars to their employees and has been quoted by Newsweek, Money magazine, the New Yorker, U.S. News & World Report, Business Week, Kiplingers, MSN Money, and several newspapers and financial industry magazines.

Ray can be contacted to answer questions or arrange speaking engagements.

Net Worth Advisory Group

9980 South 300 West, Suite 110

Sandy, Utah 84070

801-56MONEY (801-566-6639)

ray@networthadvice.com

www.networthadvice.com

J ana LeVitre-Thanks for your neverfailing support and unwavering confidence in me. Without your constant willingness to endure my often over-zealous, entrepreneurial spirit, this book would never have come to fruition. Thanks for believing with me that even the loftiest goals can be achieved and for making me want to be better than I am. Also, thanks for your tireless hours of editing and feedback.

Ray and Judy LeVitreYou are truly great parents. Thanks for your encouragement and support. A special thanks for helping me over the hurdles that life has thrown my way. Lifes challenges are much easier to face when your parents and family are always there for you. I love you for always believing in my dreams.

Chuck L. CutlerYou are a rock-solid mentor and role model. Thanks for giving me a solid financial planning foundation. Without your help I would have missed out on many opportunities and would surely not be where I am today. I owe you a great deal.

Eugene BanksBecause you hired me and gave me the opportunity to work for the largest brokerage company in the world, I owe much of what I have learned in the financial services industry to you.

My clientsA special thanks to each of you for placing so much trust in me as your financial advisor and for giving me the opportunity to help you develop a strategy to reach your financial goals. The strategies outlined in 20 Retirement Decisions You Need to Make Right Now are a culmination of my experience in working to develop fundamentally sound solutions to your unique financial situations.

And finally, I would like to thank the many companies that have invited me onto their corporate campuses and into their work sites to teach their employees how to manage a retirement-plan distribution and develop a solid investment strategy.

I f you are reading this book you are likely retiring right now. So, congratulations are in order. CONGRATULATIONS! From now on every day is Saturday.

I have spent the past twenty years helping people successfully make the financial transition from the workforce into retirement. This book is a culmination of my experience with my clients.

During my time in the financial services industry I have worked for some of the biggest and most well known financial institutions in the United States. While I am grateful to each of these firms for the employment opportunities they provided, I think that their business models are severely flawed. They seem to be much more concerned with making money for themselves rather than making money for their clients. You should be aware of the conflicts of interest that exist in the financial services industry as you seek financial advice and buy financial products at retirement. Making a mistake now could negatively impact the way you live for the next thirty to forty years. Here are some words of warning and some advice to follow as you make the financial transition from the workforce into retirement.

Most people have the need for a financial advisor to help them make money decisions at retirement. The problem with this is that most financial advisors work on commissions and have a hidden agenda to sell something. While most are well-meaning, keeping their jobs ultimately means theyve got to make a commission. In their intense efforts to meet sales quotas and pay their mortgages, they wind up pitching loaded financial products (mutual funds, annuities, and life insurance) to make a quick buck. If this occurs you will wind up with investments and insurance that are best for your advisor and his/her firm and not necessarily what is best for you. Read chapter 3, Fire Your Broker!, to see how to find objective advisors who are more interested in your goals than in theirs.

The investment and insurance products sold by commissioned advisors are expensive. When you buy loaded (i.e. commissioned) financial products, the product sponsors simply build in additional up-front, back-end, and annual expenses so they can compensate your advisor. Since these fees are often hidden, most investors never really know what they are paying. You can read chapter 18, No-Load Means Lower Costs, to learn how to avoid excessive fees.

Because commissioned advisors are under such extreme pressure to make money for their firms, they have to keep finding new clients and selling more expensive products. This is a problem. When an advisor is focused on acquiring new clients, little time remains for existing clients. The bottom line is that most people receive poor to no service from their advisors. Unfortunately, this is accepted as the norm, thus advisors are not held to higher standards. As an investor you should know what you are paying in fees (both those seen and those hidden) and make sure your advisor is providing service equal to the fees you are paying.

Font size:

Interval:

Bookmark:

Similar books «20 retirement decisions you need to make right now»

Look at similar books to 20 retirement decisions you need to make right now. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book 20 retirement decisions you need to make right now and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.