Jon Danielsson - The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It

Here you can read online Jon Danielsson - The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2022, publisher: Yale University Press, genre: Science. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It

- Author:

- Publisher:Yale University Press

- Genre:

- Year:2022

- Rating:3 / 5

- Favourites:Add to favourites

- Your mark:

The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

Finance plays a key role in the prosperity of the modern worldbut it also brings grave dangers. We seek to manage those threats with a vast array of sophisticated mathematical tools and techniques of financial risk management. Too often, though, we fail to address the greatest riskthe peril posed by our own behavior.

Jn Danelsson argues that critical risk is generated from within, through the interactions of individuals and perpetuated by their beliefs, objectives, abilities, and prejudices. He asserts that the widespread belief that risk originates outside the financial system frustrates our ability to measure and manage it, and the likely consequences of new regulations will help alleviate small-scale risks but, perversely, encourage excessive risk taking. Danelsson uses lessons from past and recent crises to show that diversity is the best way to safeguard our financial system.

Jon Danielsson: author's other books

Who wrote The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It? Find out the surname, the name of the author of the book and a list of all author's works by series.

The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

The Illusion of Control

Why Financial Crises Happen, and What We Can (and Cant) Do about It

Jn Danelsson

Yale UNIVERSITY PRESS

New Haven & London

Published with assistance from the Louis Stern Memorial Fund.

Copyright 2022 by Jn Danelsson.

All rights reserved.

This book may not be reproduced, in whole or in part, including illustrations, in any form (beyond that copying permitted by Sections 107 and 108 of the U.S. Copyright Law and except by reviewers for the public press), without written permission from the publishers.

Yale University Press books may be purchased in quantity for educational, business, or promotional use. For information, please e-mail (U.K. office).

Set in Galliard type by Newgen North America.

Printed in the United States of America.

Library of Congress Control Number: 2021948855 ISBN 978-0-300-23481-7 (hardcover : alk. paper)

A catalogue record for this book is available from the British Library.

This paper meets the requirements of ANSI/NISO Z39.48-1992 (Permanence of Paper).

10 9 8 7 6 5 4 3 2 1

Contents

Acknowledgments

Several friends and colleagues made invaluable contributions to the book. I borrowed many arguments from joint work with Charles Goodhart, Kevin James, Robert Macrae, Andreas Uthemann, Marcela Valenzuela, Ilknur Zer, and Jean-Pierre Zigrand.

I had the privilege of consulting several experts, including Peter Andrews, formerly of the FCA, Jon Frost at the Bank for International Settlements, risk system expert Rupert Goodwin, fund manager Jacqueline Li, Eric Morrison from the FCA, physicist Donal OConnell, and three lawyers: Gestur Jonsson, Haflii Kristjn Lrusson, and Eva Micheler.

I was fortunate to employ several excellent London School of Economics (LSE) students to assist me on background research for the book: Sophia Chang, Jia Rong Fan, and Morgane Fouche. Our manager at the Systemic Risk Centre, Ann Law, was very helpful in getting the book under way. The many drawings in the book were made by two excellent artists, Lukas Bischoff and Ricardo Galvao.

Without all of these people, this book would not have seen the light of day.

I am grateful to the Economic and Social Research Council (UK), grant number: ES/K002309/1 and ES/R009724/1, and the Engineering and Physical Sciences Research Council (UK), grant number EP/P031730/1, for their support.

Riding the Tiger

The man who didnt trust the models saved the world.

Figure 1. Credit: Copyright Ricardo Galvo.

Almost every economic outcome we care about is long term. Pensions, the environment, crises, real estate, education, you name it, what matters is what happens years and decades hence. Day-to-day fluctuations dont matter to most of usthe short run isnt very important. So it stands to reason that the way we manage our financial lives should emphasize the long run. But by and large, it doesnt. We are good at managing todays risk but at the expense of ignoring the promises and threats of the future. That is the illusion of control.

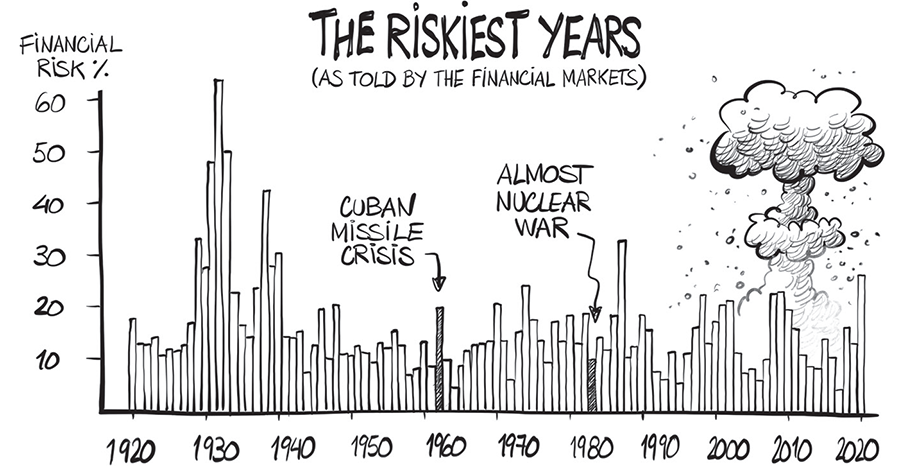

A quick test. What do you think are the riskiest years of the past century? Covid in 2020? The global crisis in 2008? The Great Depression in the 1930s? Lets ask the financial markets and their go-to measurement of ).

But these are not the riskiest years by a long shot. In 1962 and 1983 we were almost hit by the ultimate tail event, even though the financial markets remained calm. The Cuban missile crisis nearly brought the United States and the Soviet Union to blows in 1962, only for the Soviets to back down at the last minute. Even more interesting is 1983 because that is when we almost got into a nuclear war, even if we didnt know that until much later.

What happened was that the premier of the Soviet Union, Yuri Andropov, got it in his head that the United States was planning to launch a preemptive nuclear strike. He instructed his spies to find evidence supporting his suspicion, and KGB agents everywhere went into overdrive, looking for that evidence. Careers depended on it. If you have a choice of a juicy posting in Washington or being literally sent to Siberia (as the KGB rep in Novosibirsk) of course you find proof. A prime example of confirmation bias. We believe something terrible will happen and find grounds to support that, even if there is no truth to it. In 1983 the early warning models of the Soviet Union detected a nuclear attack. The man on watch that night, Stanislav Petrov, didnt trust the signal and decided unilaterally not to launch a counterattack. The man who didnt trust the models saved the world. The Soviet investigators subsequently confirmed he was right. The false alarm came about because of a rare alignment of sunlight on high-altitude clouds above North Dakota and the Molniya orbits of the detection satellites. Colonel Petrov died in 2017, by that time globally recognized for having saved humanity.

The way we measure financial risk today, with what I call the riskometer, has much in common with Andropovs early warning systems. Both rely on imperfect models and inaccurate measurements to make crucial decisions. While high-altitude clouds bedeviled the Soviets models, the problem for todays riskometer arises from its emphasis on the recent past and short-term risk. The reason is simple. That is the easiest risk to measure, as the modelers have plenty of data.

The problem is that short-term risk isnt all that important, not for investors and especially not for the financial authorities. For them, what matters is systemic risk, the chance of spectacular financial crises, like the one we suffered in 2008. Long-term threats, like systemic crises or our retirement not being as comfortable as hoped for, are easy to understand, at least conceptually. Take crises. Banks have too much money and cant find productive investments, so they start lending to increasingly low-quality borrowers, often in real estate. In the beginning it looks like magic. Money flows in, developers build houses, and everybody feels rich, encouraging more lending and more building in a happy, virtuous cycle. Then it all comes crashing down.

What are we to do? Regulation, of course, using the Panopticon. An idea dating to the eighteenth-century English philosopher Jeremy Bentham, who proposed regulating society by setting up posts to observe human activity. Does it work? In traffic certainly. If no police or cameras monitor speeding, I suspect many will be tempted to drive too fast. The chance of getting caught keeps the roads relatively safe. Surely we can also employ the Panopticon to regulate finance and so prevent crises and all the horrible losses. We do use it, but it doesnt work all that well. The reason has to do with the interplay of two complex topics, the difficulty of measuring risk and human ingenuity.

Unlike temperature or prices, risk cannot be directly observed. Instead, it has to be inferred by how prices have moved in the past. That requires a model. And as the statistician George Box had it, All models are wrong, but some are useful. There are many models for measuring risk, they all disagree with each other, and there is no obvious way to tell which is the most accurate. Even then, all the riskometers capture is the short term because that is where the data is.

And then we have human behavior. Hyman Minsky observed forty years ago that stability is destabilizing. If we think the world is safe, we want to take on more risk, which eventually creates its own instability. And since the time between decisions and bad things happening can be years or decades, it is hard to control risk. As my coauthor Charles Goodhart put it, Any observed statistical regularity will tend to collapse once pressure is placed upon it for control purposes. What Goodharts law tells us is that when the risk managers start controlling risk, we tend to react in a way that makes the risk measurements incorrect.

Font size:

Interval:

Bookmark:

Similar books «The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It»

Look at similar books to The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book The Illusion of Control: Why Financial Crises Happen, and What We Can (and Cant) Do About It and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.