Duane Milano - Accounting I Essentials

Here you can read online Duane Milano - Accounting I Essentials full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2012, publisher: INscribe Digital;Research & Education Association, genre: Children. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Accounting I Essentials

- Author:

- Publisher:INscribe Digital;Research & Education Association

- Genre:

- Year:2012

- Rating:4 / 5

- Favourites:Add to favourites

- Your mark:

Accounting I Essentials: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Accounting I Essentials" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

REAs Essentials provide quick and easy access to critical information in a variety of different fields, ranging from the most basic to the most advanced. As its name implies, these concise, comprehensive study guides summarize the essentials of the field covered. Essentials are helpful when preparing for exams, doing homework and will remain a lasting reference source for students, teachers, and professionals. Accounting I includes accounting principles, the accounting cycle, adjusting entries, closing entries, worksheet procedures, accounting for a merchandising operation, internal control and specialized journals, cash, receivables, inventory, property, plants and equipment, and long-term assets.

Duane Milano: author's other books

Who wrote Accounting I Essentials? Find out the surname, the name of the author of the book and a list of all author's works by series.

Accounting I Essentials — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Accounting I Essentials" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

Accounting can be described as an information system that provides essential information about the financial activities of a business entity to various individuals or groups for their use in making informed decisions.

Accounting is primarily concerned with the design of the recordkeeping system, the preparation of summarized reports based on the recorded data, and the interpretation of those reports.

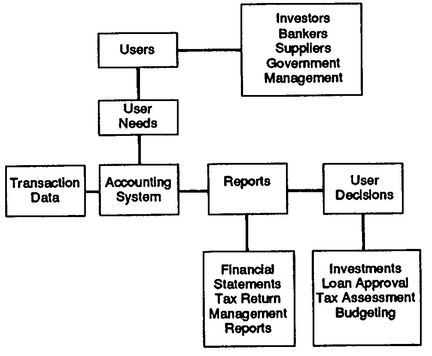

Users of accounting information can be quite varied, depending on the type of decision under consideration. Accounting information might be used for decisions involving investments, to impose income taxes, or for regulatory or managerial decisions. The process of using accounting to provide information to users is illustrated in Chart 1.2.1.

As shown in this diagram, the first step is to identify user needs. A properly designed accounting system can then generate summarized reports (using recorded transaction data) to meet those needs for accounting information. Users can then use those reports to make informed business decisions.

CHART 1.2.1

This broad range of potential users has brought about the evolution of Generally Accepted Accounting Principles (GAAP) used in preparation of financial statements. Many of these principles have been formally established by standard-setting bodies such as the Financial Accounting Standards Board (FASB). Others have simply gained acceptance through widespread use. Adherence to GAAP provides a measure of consistency in preparation of financial statements.

Assets are tangible or intangible properties owned by a business. The rights or claims to those assets are equities. Owners and creditors provide resources that enable a business to purchase assets and therefore are said to have equity in that business. For instance, an owner may start a business with $10,000 cash. This cash is used to buy equipment. The owner, who provided the funds for the equipment, has a claim to that equipment.

The relation between assets and equities is shown by the equation:

Assets = Equities

Equities can be subdivided into two categories: (1) Liabilities : rights of creditors represented by debts of the business, and (2) Owners Equity : rights of the owner or owners.

Expanding the original equation by using the two categories of equities shown in 1.4 yields the accounting equation :

Assets = Liabilities + Owners Equity

Creditors have preferential rights to the assets of a corporation. The residual claim of the owner or owners may be better understood by restating the accounting equation as:

Assets Liabilities = Owners Equity

The dollar totals of both sides of the accounting equation are always equal, since they are simply two views of the same business property. The list of assets provides a description of the various business properties, while the list of liabilities and equity indicates the funding source for those assets.

A transaction can be defined as an occurrence or an event that must be recorded. Any business transaction can be stated in terms of the resulting change in the three basic elements of the accounting equation. The equality of the two sides of the accounting equation must be maintained upon completion of a transaction.

As an illustration, examine the result of a transaction to purchase land for $10,000 cash.

Assets (+$10,000 land $10,000 cash) =

Liabilities + Owners Equity

In this case, assets would be increased by $10,000 to reflect the land purchase and decreased by $10,000 to reflect cash paid. The net effect on assets is zero, so the accounting equation remains valid.

As another example, modify the transaction above to reflect the purchase of land by borrowing $10,000 purchase price with a bank loan (also known as a note payable).

Assets (+$10,000 land) = Liabilities (+$10,000 note payable) + Owners Equity

In this case, assets and liabilities are each increased by $10,000. The accounting equation therefore remains in balance.

As defined in 1.1, one of the major concerns of accounting is the preparation of summarized reports of recorded data. The principal statements used to communicate summarized data are the income statement, the statement of owners equity, and the balance sheet. A brief description of each statement follows:

A summary of the revenue and expenses of a business entity for a specific period of time, such as a month or a year. If total revenues for the period in question exceed total expenses, the result is net income (or net profit). If total expenses exceed total revenues, the result is a net loss.

A summary of the changes in the owners equity of a business entity for a specific period of time, such as a month or a year. In a corporation, the emphasis is on reports of changes in retained earnings (net income retained in the business). Those changes are reported in the retained earnings statement.

A list of the assets, liabilities and owners equity of a business entity as of a specific date, usually at the close of the last day of a month or a year. Assets are usually listed first, followed by a list of liabilities and a section detailing owners equity. Asset accounts (known as the left-hand side of the balance sheet) carry debit balances. Assets are usually listed with cash first, followed by accounts receivable, inventory, and other assets considered to be current assets (those easily converted to cash or expected to be converted to cash within one year). These are subtotaled and followed by a list of long-term assets such as land and equipment.

Liabilities are classified similarly. Current liabilities (those due within one year) are listed first, usually in the order of accounts payable, notes payable, and various other obligations such as salaries payable. These are subtotaled and followed by a listing of long-term liabilities (those due after one year). Liabilities and owners equity (known as the right-hand side of the balance sheet) carry credit balances. reflects the proper classification of accounts and balance sheet format.

Font size:

Interval:

Bookmark:

Similar books «Accounting I Essentials»

Look at similar books to Accounting I Essentials. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Accounting I Essentials and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.