Duane Milano - Accounting II Essentials

Here you can read online Duane Milano - Accounting II Essentials full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2012, publisher: INscribe Digital;Research & Education Association, genre: Children. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Accounting II Essentials

- Author:

- Publisher:INscribe Digital;Research & Education Association

- Genre:

- Year:2012

- Rating:4 / 5

- Favourites:Add to favourites

- Your mark:

Accounting II Essentials: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Accounting II Essentials" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

REAs Essentials provide quick and easy access to critical information in a variety of different fields, ranging from the most basic to the most advanced. As its name implies, these concise, comprehensive study guides summarize the essentials of the field covered. Essentials are helpful when preparing for exams, doing homework and will remain a lasting reference source for students, teachers, and professionals. Accounting II includes current liabilities, long-term liabilities, bonds, partnerships, corporations, earnings and dividends, consolidations, statement of cash flows, and financial statement analysis.

Duane Milano: author's other books

Who wrote Accounting II Essentials? Find out the surname, the name of the author of the book and a list of all author's works by series.

Accounting II Essentials — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Accounting II Essentials" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

(a sample of the hundreds of letters REA receives each year)

Your Essentials books are great! They are very helpful, and have upped my grade in every class. Thank you for such a great product.

Student, Seattle, WA

I recently purchased six titles from your history Essentials series and I find them to be excellent.

Student, Dublin, Ireland

Thank you for volumes I & II of The Essentials of Statistics. I am very pleased with these two little booklets.

Student, Portland, OR

The Essentials book always comes to the rescue.

Student, Norwood, MA

Ive had the pleasure of using your Essentials of Physics study guide books, and have found them to be very helpful.

Student, Minneapolis, MN

Current liabilities are those obligations which must be paid within one year. This includes the portion of long-term debt that is due and payable within one year. Common types of current liabilities include accounts payable, notes payable, accrued liabilities for wages or interest as well as estimated liabilities such as income taxes.

Accounts payable arise when a business purchases inventory or equipment on a credit basis. An example of the journal entry to reflect the purchase of inventory on credit is shown in Example 13.2.1.

The Sample Company

General Journal

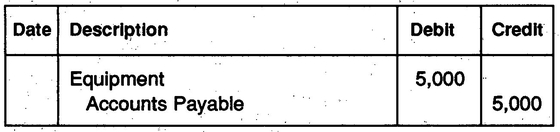

The use of the purchases account is limited strictly to purchases of Inventory on credit. Purchases of other items would be reflected as affecting those accounts directly. As an example, if equipment were purchased on account, the journal entry to reflect that is shown in Example 13.2.2.

The Sample Company

General Journal

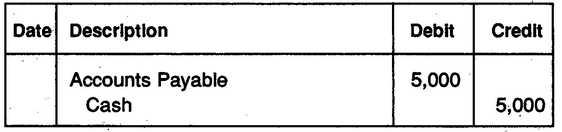

Payment of those payables are recorded as a debit to accounts payable and a credit to cash as shown in Example 13.2.3.

The Sample Company

General Journal

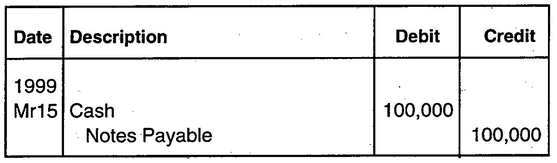

Notes payable occur when a business borrows money. Business transactions such as the purchase of real estate or equipment, as well as a temporary need for additional working capital, may necessitate such borrowings. As an example, assume that on March 15, 1999, Smith Corporation borrows $100,000 from its bank for 90 days. Interest is payable at maturity and accrues as a rate of 12%. The journal entry to record this transaction is shown in Example 13.3.1.

The Sample Company

General Journal

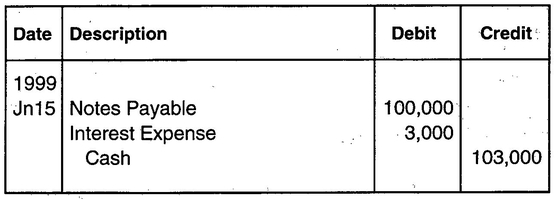

On June 15, 1999, Smith Corporation repaid the loan plus $3,000 interest ($100,000 12% 90/360). In this instance, a 360-day year is used for interest calculation. The journal entry to record this transaction is shown in Example 13.3.2.

The Sample Company

General Journal

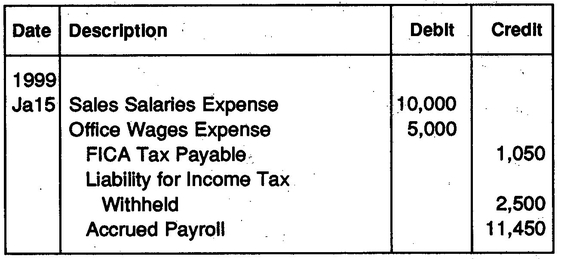

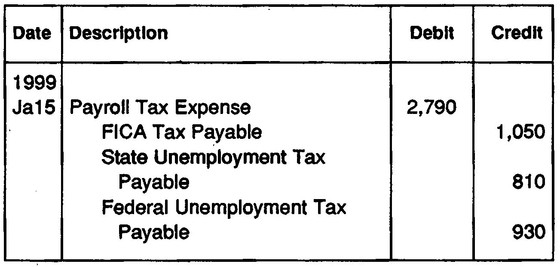

Employees are rarely paid on a daily basis. Instead, a business accrues liability for payroll between pay dates (usually bi-weekly). The gross amount of wages is relatively easy to calculate, consisting of hours worked multiplied by the hourly wage. Salaries are paid bi-weekly or monthly based on some present annual amount. Employers are also responsible for withholding a portion of gross pay for social security (FICA) and Federal income taxes. In addition, the employer may withhold State and municipal income taxes (if applicable). Example 13.4.1 reflects the journal entry necessary to record payroll expense and liabilities as of January 15, 1999 (the end of the payroll period).

The Sample Company

General Journal

In this example, although the business has incurred $15,000 in total salary and wages expenses, only $11,450 is actually paid out to employees. The remainder will be submitted to the appropriate government agency at regular intervals. Other withholdings, such as union dues, would be handled similarly.

At the same time, an employer incurs liabilities for certain payroll taxes. These include FICA tax (figured at the same rate and on the same amount of earnings as the employees), Federal unemployment tax, and State unemployment tax. The journal entry to record the employers tax expense and liabilities is reflected in Example 13.4.2.

The Sample Company

General Journal

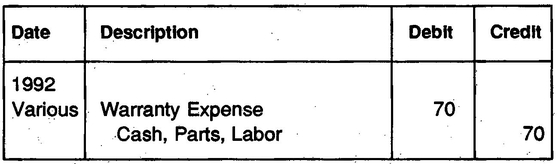

A business may have liabilities that, while quite real, can only be estimated. A company which sells appliances with warranties can incur this kind of liability. In such situations, the company guarantees free repair within a specified period of time in the event of a problem with their product.

The estimate of the probable expense of such repairs may be based on prior experience. In such a case, the liability for warranties might be a percentage of total sales in a given period. For example, assume the Sample Company sells 200 refrigerators in 1992 with one year warranties. Based on past experience, the company expects 5% of its refrigerators to be defective within the one year warranty period. The average service call is estimated at $25. During 1992, 3 refrigerators are repaired at a total cost of $70. In 1993, 6 refrigerators are repaired at a cost of $130. Example 13.5.1 reflects the entries necessary to record expenditures for repairs as well as the entry to estimate warranty liability. Note that warranty expense is incurred in the accounting period when the refrigerators are sold, not when the repairs are made.

Font size:

Interval:

Bookmark:

Similar books «Accounting II Essentials»

Look at similar books to Accounting II Essentials. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Accounting II Essentials and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.