Jessica Irvine - Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting

Here you can read online Jessica Irvine - Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting full text of the book (entire story) in english for free. Download pdf and epub, get meaning, cover and reviews about this ebook. year: 2022, publisher: Wiley, genre: Romance novel. Description of the work, (preface) as well as reviews are available. Best literature library LitArk.com created for fans of good reading and offers a wide selection of genres:

Romance novel

Science fiction

Adventure

Detective

Science

History

Home and family

Prose

Art

Politics

Computer

Non-fiction

Religion

Business

Children

Humor

Choose a favorite category and find really read worthwhile books. Enjoy immersion in the world of imagination, feel the emotions of the characters or learn something new for yourself, make an fascinating discovery.

- Book:Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting

- Author:

- Publisher:Wiley

- Genre:

- Year:2022

- Rating:5 / 5

- Favourites:Add to favourites

- Your mark:

Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting: summary, description and annotation

We offer to read an annotation, description, summary or preface (depends on what the author of the book "Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting" wrote himself). If you haven't found the necessary information about the book — write in the comments, we will try to find it.

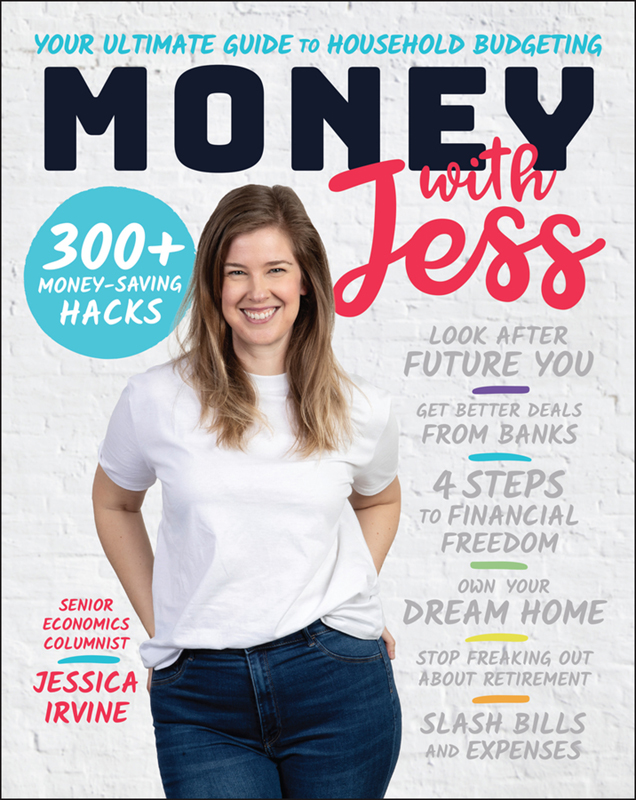

**Winner of the Book of the Year, Winner of the Personal Development Book of the Year and Finalist of the Finance and Investment Book of the Year at the Australian Business Book Awards 2022**

Learn how to get money, how to spend it and how to save it.

Does thinking about money make you feel overwhelmed, confused or anxious? That ends now. Join one of Australias most loved and respected economics journalists, Jessica Irvine, as she helps you strip away your negative money thoughts and teaches you the real meaning of money: how to get it, how to spend it and how to save it.

Whether you want to buy a home, retire comfortably, sleep well at night, leave a job you hate or borrow to build your wealth, learning to budget your money is the foundation of all good money decisions.

Money with Jess unpacks the unique and simple system Jess created for organising, tracking and investing her own money. Youll also find:

Money doesnt have to be intimidating. With Money with Jess, you can forget the fear and learn to make money decisions with confidence.

Jessica Irvine: author's other books

Who wrote Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting? Find out the surname, the name of the author of the book and a list of all author's works by series.

Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting — read online for free the complete book (whole text) full work

Below is the text of the book, divided by pages. System saving the place of the last page read, allows you to conveniently read the book "Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting" online for free, without having to search again every time where you left off. Put a bookmark, and you can go to the page where you finished reading at any time.

Font size:

Interval:

Bookmark:

First published in 2022 by John Wiley & Sons Australia, Ltd

42 McDougall St, Milton Qld 4064

Office also in Melbourne

Jessica Irvine 2022

The moral rights of the author have been asserted.

ISBN: 9780730398233

All rights reserved. Except as permitted under the Australian Copyright Act 1968 (for example, a fair dealing for the purposes of study, research, criticism or review), no part of this book may be reproduced, stored in a retrieval system, communicated or transmitted in any form or by any means without prior written permission. All inquiries should be made to the publisher at the address above.

Cover design by Wiley

Author photos: Louie Douvis

Cover background image: silverpak/Shutterstock

Title hand lettering image: veryvery/Shutterstock

Lightbulb image: Dashk/stock.adobe.com

Arrow image and notebook image: Anatoliy Babiy/iStock

Highlighter image: OpenClipartVectors from Pixabay.

Disclaimer

The material in this publication is of the nature of general comment only, and does not represent professional advice. It is not intended to provide specific guidance for particular circumstances and it should not be relied on as the basis for any decision to take action or not take action on any matter which it covers. Readers should obtain professional advice where appropriate, before making any such decision. To the maximum extent permitted by law, the author and publisher disclaim all responsibility and liability to any person, arising directly or indirectly from any person taking or not taking action based on the information in this publication.

If you are in financial distress, call the National Debt Helpline on 1800 007 007 on weekdays between 9.30 am and 4.30 pm (Australia only).

An army of trained financial counsellors is standing by to help you negotiate with creditors (people you owe money to) and to help get you back on financial track.

It's a completely free, independent and confidential service funded by the government and delivered by notforprofit organisations in your state.

You can also access a live chat feature on their website: ndh.org.au.

Throughout this book, I refer to many worksheets I have created to help you get started on your budgeting journey. All the resources I refer to are available to download for free from my website: jessicairvine.com.au.

Check it out and get downloading today!

For Henry xx

Hello friends!

My name is Jess and I'm good at money. Like, really good.

It's taken a long time for me to be able to say that with confidencepartly because it wasn't always true.

Shortly after I divorced in my mid30s, a colleague suggested I write a book titled A Man Is Not a Financial Plan about how to manage your finances as a single parent. Trouble was, I didn't know how.

Which is a bit embarrassing, really, given I've now been working as a highprofile economics and finance journalist for some of Australia's most prestigious newspapers for the better part of two decades.

I have a university degree in economics and philosophy. It's my job to regularly pass judgement on how the nation's treasurer is managing the country's budget. I've reported on 18 annual federal budgets so far (not counting the bonus emergency budgets and stimulus packages during the Global Financial Crisis and COVID19).

I've interviewed prime ministers on live TV, enjoyed private oneonone lunches with Reserve Bank governors and I regularly text and speak with treasury secretaries, both past and present.

I've been to budgeting nerd paradise'as the 1970s chanteuse Charlene once famously (almost) sangbut I'd never, until quite recently, taken a very serious look at my own personal finances.

It's not that I was ever particularly bad at money, depending on your definition of this. I've never had a credit card I couldn't pay off in full each month to avoid paying interest. And I've always paid my bills on time.

But, wow, have I spent a lot of money during my 40 years on this earth!

As my career blossomed in my late 20s and early 30s, I thought nothing of dropping $400 on a new designer suit jacket, a meal at a posh restaurant or a night at a fancy hotel.

I remember spending about that much to have my childhood copy of The Lord of the Rings rebound in an expensive, fabricclad hard cover by a specialist antique book store.

Pretty cool, right?

But then, one day, you find yourself pushing 40 as a divorced single mum who doesn't own a home, has never invested in shares or property and has no idea if she's on course for a comfortable retirement.

I'm the classic example of someone who knows a lot about something in theory, but was pretty crap at applying it in practice.

Looking back, I can see that at the time of my colleague's bookwriting suggestion, I was still drowning in deep shame and sadness at the failure of my marriage and my single parenthood.

But, as the dust began to settle on my new life, I did start to slowly pick myself up and put my financial life togetherperhaps for the first time.

I bought my first home as a single mum aged 38 (I share all my best hacks for navigating that gruelling process in stay tuned!).

At about that time, I began writing a weekly personal finance column for the Money sections of the Sunday Age and Sun Herald newspapers. In it, I finally began applying all the economic theory I had learned to overhauling my reallife financesand sharing all the gory details with readers.

My Instagram account, @moneywithjess, began to grow rapidly and I pitched the idea of a weekly email newsletter of the same nameMoney with Jessto share the results of my onewoman mission to budget, save and invest.

You name a crazy moneysaving experiment, I've tried it!

I once kept a spreadsheet to calculate the precise cost of every meal I cooked for one week to figure out a realistic food budget (it worked out about $85 per week for me and my son). I used another spreadsheet to tally the cost of buying the same basket of groceries from two different supermarkets to find out which was cheaper (spoiler alert: Aldi).

I kept a handwritten tally on a sticky note stuck to a bottle of dishwashing powder to figure out the perwash cost and whether it is cheaper than using tablets (it is, mostly because you can just use less detergent).

I didn't buy any clothes for an entire year. I cut my own hair. I gave up getting blonde foils (you can just see the remnant of my former colour on the tips of my hair in the cover photo for this book).

I began meticulously tracking my spending and in one article published the details of every single dollar I spent in one financial year (I know you'll want to know: it was $88379.84 in 202021).

Bigger picture: I embarked on an epic hunt for the best mortgage deal, locking in my interest rate in for two years at 1.84 per cent and scoring a $4000 cash back for my efforts.

I began making regular voluntary contributions to my retirement savings account.

And finally, in May 2021, I did something I had never previously dreamed of. I began investing directly in the share market for the first timesomething I continue to do on a regular monthly basis and will tell you about in .

Next pageFont size:

Interval:

Bookmark:

Similar books «Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting»

Look at similar books to Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting. We have selected literature similar in name and meaning in the hope of providing readers with more options to find new, interesting, not yet read works.

Discussion, reviews of the book Money with Jess: Award-winning Book of the Year: Your Ultimate Guide to Household Budgeting and just readers' own opinions. Leave your comments, write what you think about the work, its meaning or the main characters. Specify what exactly you liked and what you didn't like, and why you think so.